Deriv cTrader Volatility Indices explained

Volatility refers to the speed and magnitude of market movements. It shapes every trader’s perception of risk and reward. On Deriv, volatility takes a unique form through synthetic indices — algorithmically generated markets that mimic real-world price behaviour without being affected by macroeconomic news or liquidity shifts.

In 2025, Deriv extended its innovation with the launch of fifteen new volatility and Crash/Boom indices on Deriv cTrader. These one-second tick instruments enable faster execution, finer control over volatility regimes, and seamless integration with automated systems such as cBots and Expert Advisors (EAs). Together, they expand Deriv’s reputation as a trusted provider of transparent, data-driven synthetic markets.

These indices are designed for precision and consistency. They enable traders to test, refine, and automate strategies in a stable environment that operates 24/7, free from external disruptions — ideal for both educational purposes and testing automated strategies.

Quick summary

- Volatility indices replicate markets with fixed volatility levels (e.g., 15%, 30%, 90%) or defined event probabilities (e.g., one Boom or Crash every 600 ticks).

- They run continuously and are unaffected by real-world events, creating a controlled testing ground for traders and developers.

- Deriv launched seven new Deriv cTrader-exclusive indices: Volatility 15, 30, and 90 (1s), plus Boom 600, Crash 600, Boom 900, and Crash 900, offering faster tick speeds and broader volatility coverage.

- Demo access began 4 January 2024, with live trading available from 11 January 2024.

- The 1-second series bridges traditional volatility concepts such as the CBOE Volatility Index (VIX) with synthetic consistency, allowing traders to plan around predictable volatility “regimes.”

What are synthetic indices, and how can traders use them?

Deriv’s synthetic indices are markets generated by cryptographically-secure algorithms that produce consistent statistical characteristics. Each index either maintains a fixed volatility level or follows a stochastic pattern that defines the probability of sharp price events, such as spikes or drops.

They provide continuous data streams and are ideal for studying market behaviour, developing automated strategies, and teaching volatility management in isolation from real-world variables. A trader using Volatility 30 (1s) can receive approximately 86,400 ticks per day, allowing for precise backtesting and automation insights.

This reliability enables structured learning and automated strategy testing within controlled volatility regimes, which is a crucial component of Deriv’s synthetic markets ecosystem.

Why do volatility indices matter for Deriv traders?

Deriv’s latest expansion marks a key milestone in the evolution of synthetic trading. It extends the company’s vision of creating advanced tools for both discretionary and algorithmic traders.

According to Prakash Bhudia, Deriv’s Head of Product & Growth:

“The new indices amplify opportunities by giving traders faster, cleaner access to volatility patterns — without needing complex technical setups.”

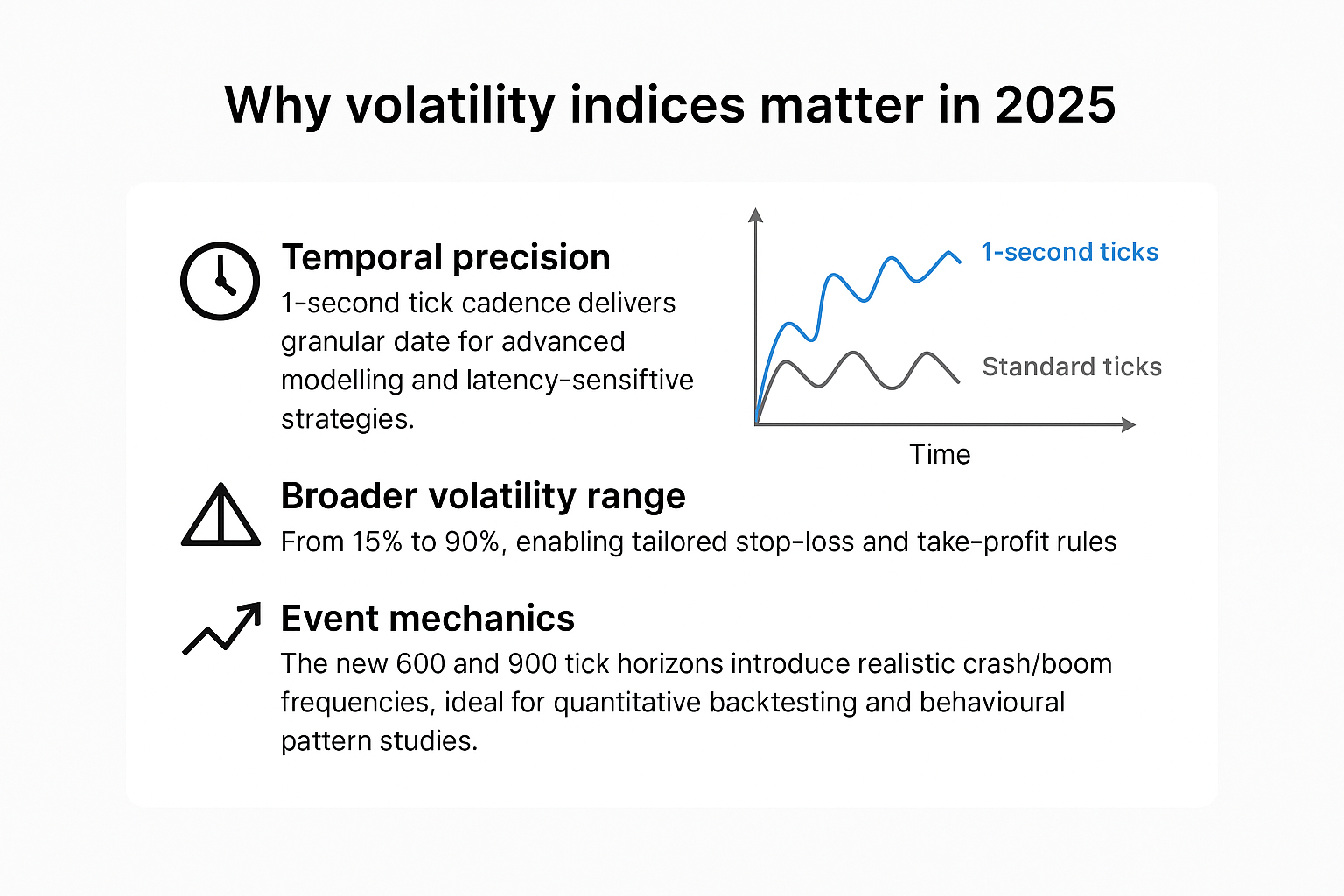

Three innovations define this release:

- Temporal precision: A one-second tick cadence delivers granular data for advanced modeling and latency-sensitive (ultra-fast execution) strategies.

- Broader volatility range: From 15% to 90%, enabling tailored stop-loss and take-profit rules.

- Event mechanics: The new 600 and 900 tick horizons introduce realistic crash/boom frequencies, ideal for quantitative backtesting and behavioural pattern studies.

Together, these indices demonstrate how Deriv continues to refine synthetic markets for diverse trading and educational use cases, enabling traders to master volatility with greater control and data transparency — a perspective also supported by the IMF’s Global Financial Stability Report.

How Deriv’s volatility and Crash/Boom indices compare

Notes: “σ” denotes volatility. “Avg event frequency” represents long-term statistical averages rather than fixed timing.

This comparison highlights how each instrument fits different volatility regimes and strategy objectives, helping traders align risk exposure with trading style.

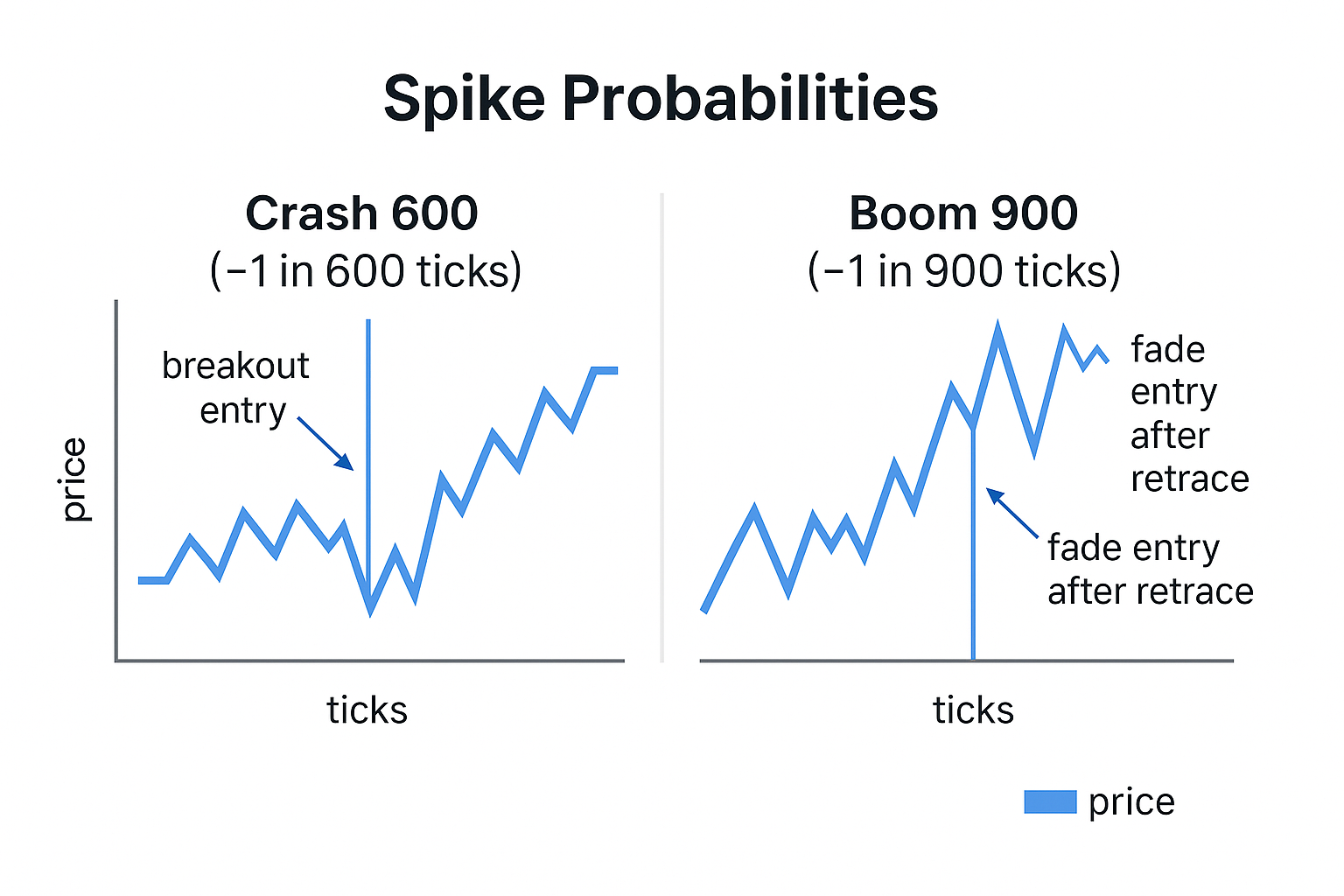

How can traders use Crash and Boom indices effectively?

Crash and Boom indices are designed to replicate sudden price movements — upward “booms” or downward “crashes.” Every tick represents a small probability of a large move.

- Crash 600: Roughly one major drop every 600 ticks.

- Boom 900: Roughly one major spike every 900 ticks.

This stochastic design allows traders to test both breakout and fade strategies:

- Breakout strategies enter when a spike begins and trail the move.

- Fade strategies trade in the opposite direction after volatility normalises.

Monitoring spike frequency and magnitude helps define realistic stop-loss levels and manage drawdown. These dynamics demonstrate how volatility regimes within synthetic markets can be applied to both educational and live-trading scenarios.

To illustrate, a trader analysing Boom 900 might expect approximately 144 major spikes in a 24-hour session (given 86 400 ticks per day ÷ 900). This quantitative expectation helps in calibrating risk and timing automation logic.

Which Deriv platforms are best for volatility trading strategies?

Deriv offers multiple platforms for different trader profiles:

- Deriv cTrader: Advanced order management, Depth of Market, and cBots automation. Ideal for 1-second indices and 600/900 series.

- Deriv MT5: Multi-asset environment supporting EAs, hedging, and indicator libraries. Best for combining synthetics with forex, crypto, and stock Contract for Difference (CFDs).

- Deriv Trader: Home of multipliers and options, providing fixed-risk control for structured trades.

- Deriv GO: Mobile app for monitoring positions and managing exposure.

- Deriv Bot: No-code automation builder for designing and deploying basic strategies without programming.

Together, these platforms form an integrated ecosystem for automated strategy testing, enabling users to migrate smoothly between manual and algorithmic trading environments.

Each platform supports integration across Deriv’s ecosystem, allowing seamless strategy migration from education to live execution.

How do synthetic indices support automated trading systems?

Synthetic indices are well-suited for automation tools due to their consistent volatility and uninterrupted price data. Traders can build, test, and optimise algorithmic strategies without external disruptions.

Common tools include:

- cBots on Deriv cTrader for custom-coded execution.

- Expert Advisors (EAs) on Deriv MT5 for cross-asset automation.

- Deriv Bot for drag-and-drop logic creation without programming skills.

Each tool allows traders to monitor and manage volatility strategies efficiently in both demo and live environments. This connected design reinforces Deriv’s focus on precision, education, and accessibility across synthetic markets.

Furthermore, automation helps traders quantify outcomes — for instance, measuring how frequently an algorithm triggers entries per tick cycle — which is invaluable for data-driven performance reviews.

What are the most effective volatility trading strategies for different regimes?

- Volatility 15 (1s): Best for micro-scalping and mean reversion. Use moving averages, RSI, and Bollinger Bands with tight stops and quick exits.

- Volatility 30 (1s): Balanced for range trading and short-term momentum. Combine MA crossovers with ATR-based stops.

- Volatility 90 (1s): Ideal for breakout systems with wide stops and structured risk buffers. Use time-based exits to prevent churn.

- Crash/Boom 600–900: Best for event-driven tactics. Traders can follow spikes (breakout) or fade them (mean reversion) using ATR trails and structured stop-loss logic.

As Rakshit Choudhary, Deriv’s CEO, notes:

“Deriv’s focus remains on advancing AI-first trading technology and empowering traders with precision tools built for the next decade.”

Jean-Yves Sireau, Deriv’s Founder, adds:

“Our synthetic markets let traders experience volatility safely, transparently, and continuously — something no traditional market can provide.”

These combined perspectives underscore how Deriv leverages human expertise and algorithmic innovation to establish new benchmarks for volatility trading.

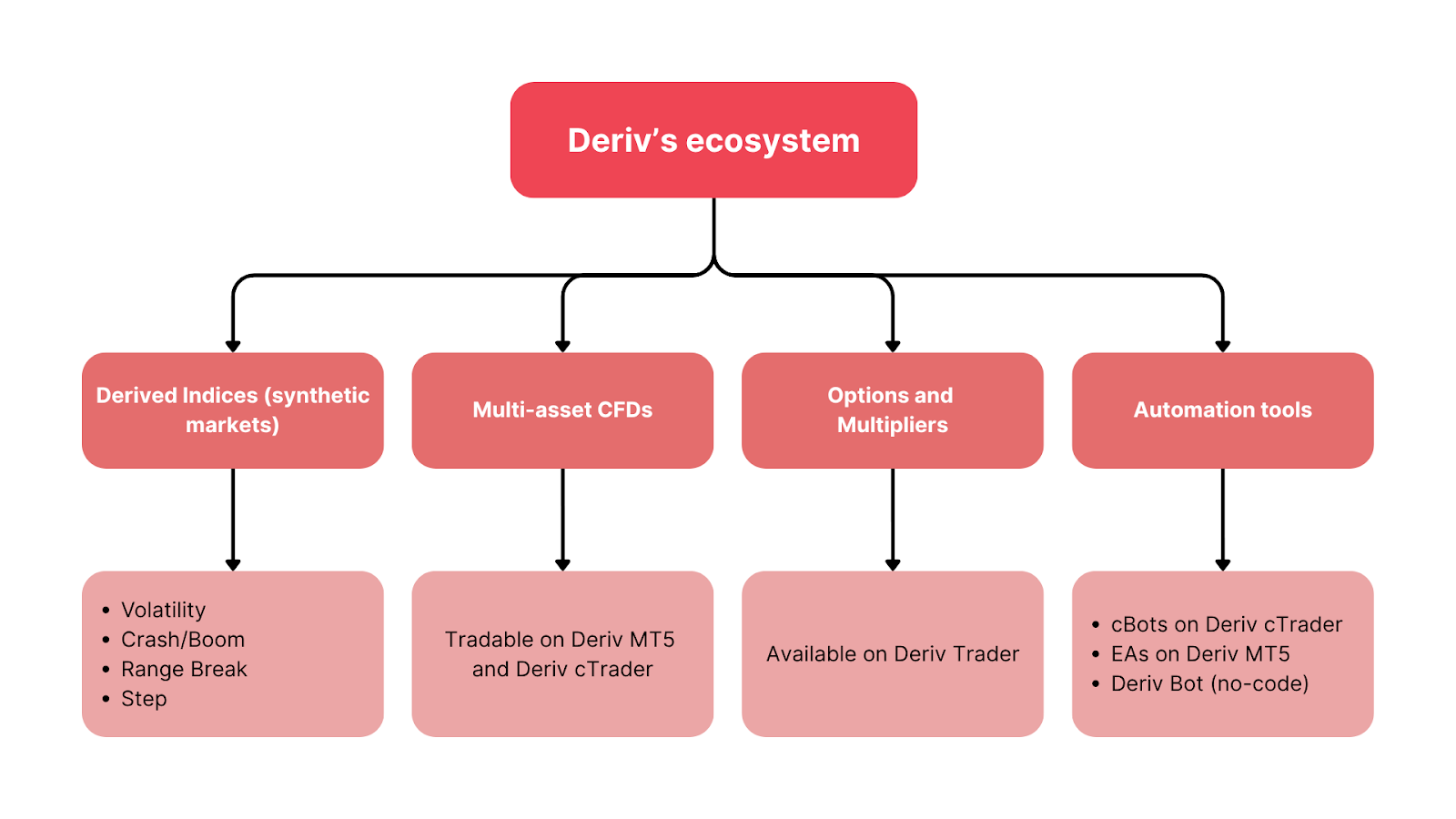

How do Deriv’s volatility indices connect across its trading ecosystem?

Deriv’s trading infrastructure links all synthetic and real-market products, creating a unified environment for experimentation, education, and automation.

- Derived Indices (synthetic markets):

- Spot Volatility

- Drift Switching

- DEX

- Volatility

- Crash/Boom

- Jump

- Step

- Range Break

- Daily Reset

- Multi Step

- Hybrid

- Skew Step

- Trek

- Volatility Switch

- Stable Spread Instruments

- Multi-asset CFDs: Tradable on Deriv MT5 and Deriv cTrader.

- Options and Multipliers: Available on Deriv Trader.

- Automation tools: cBots on Deriv cTrader, EAs on Deriv MT5, and Deriv Bot (no-code).

This structure enables traders to design, test, and scale strategies seamlessly between demo and live environments. Lessons learned on synthetics — about margin call, leverage, and drawdown — directly improve performance across asset classes.

According to independent quantitative analyst Sarah Langford, Deriv’s structured volatility ranges “simplify regime-based strategy design for retail quants.” This external validation underscores how Deriv’s synthetic markets promote analytical trading and consistent skill development.

The information contained within this blog article is for educational purposes only and is not intended as financial or investment advice.

Deriv cTrader is unavailable to clients residing within the European Union.