Is Intel’s stock gap-up the start of a sustainable rally or just a one-day spike?

.webp)

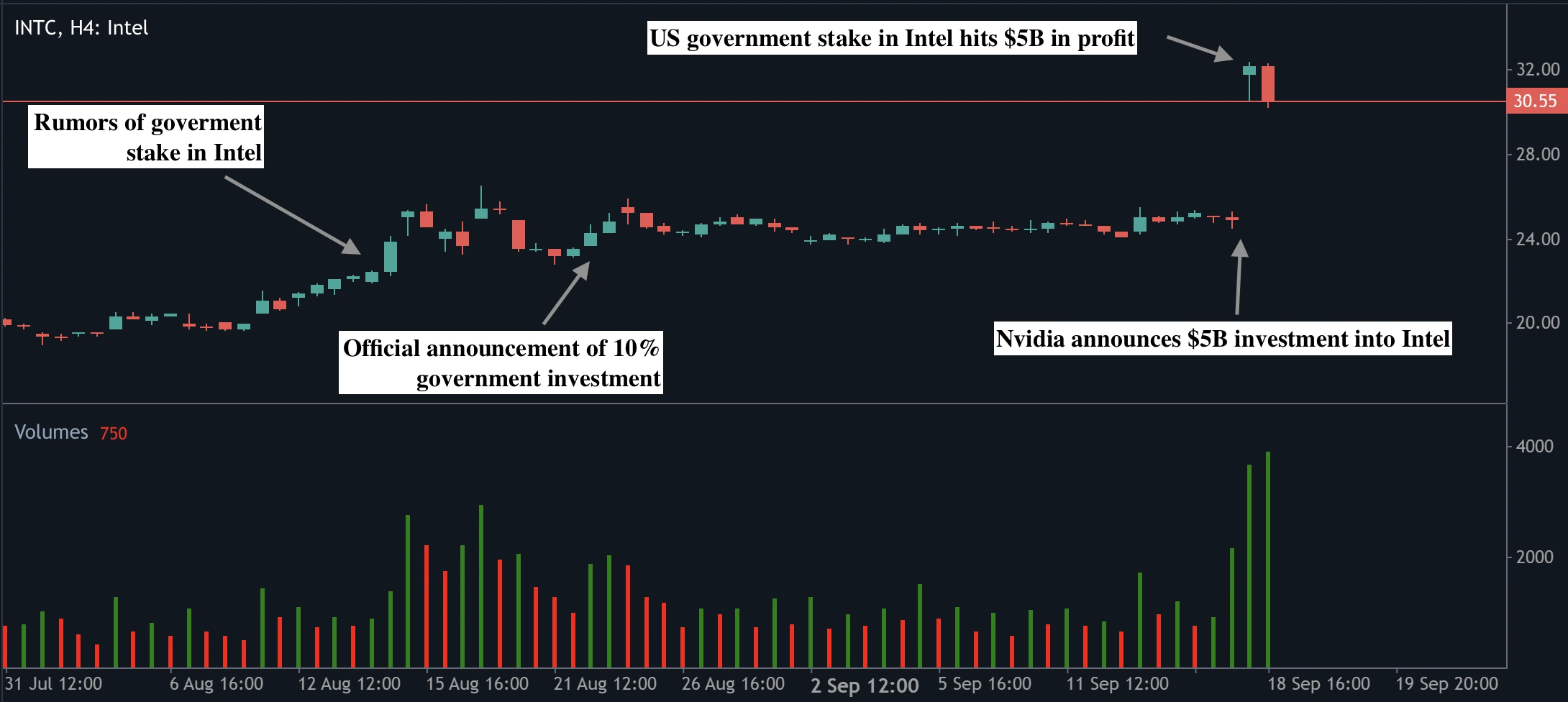

Intel’s 23% surge, its biggest one-day gain since 1987, looks more like a news-driven spike than the start of a sustainable rally, according to analysts. The stock jump was powered by Nvidia’s $5 billion investment and the U.S. government’s earlier $8.9 billion stake, lifting Intel’s market capitalisation by $23.7 billion in a single session. While political and corporate backing has given Intel fresh momentum, the company’s unprofitable foundry business and continued reliance on the Taiwan Semiconductor Manufacturing Company, mean that lasting recovery will depend on execution, not headlines.

Key takeaways

- Intel shares soared 22.77% to $30.57, their largest one-day rally in nearly four decades, adding $23.7 billion in market value.

- Nvidia purchased $5 billion in Intel stock at $23.28 per share, giving it around 4% ownership.

- The U.S. government invested $8.9 billion in August for a 10% stake, paying $20.47 a share.

- The partnership will see Intel design custom CPUs for Nvidia’s AI data centres and co-develop PC chips integrated with Nvidia GPUs.

- Intel’s foundry business remains deeply unprofitable, and both companies will continue relying on TSMC, leaving sovereignty goals unmet.

- Analysts are split: Some call it a “game-changer,” while others caution that it is a geopolitical rally without guaranteed fundamentals.

Intel’s stock rally explained: Nvidia Intel partnership

The immediate catalyst was Nvidia’s decision to invest $5 billion in Intel, buying common stock at $23.28 a share. This followed the U.S. government’s purchase of 433.3 million shares for $8.9 billion at $20.47, giving Washington close to a 10% stake. Combined, these two moves represent nearly $14 billion in fresh capital and two of the most powerful endorsements Intel could have hoped for.

The announcement was coupled with a product partnership: Intel will design custom CPUs optimised for Nvidia’s AI data centres and integrate Nvidia’s RTX GPUs into its PC chips. This joint venture pushes Intel back into growth markets it has long struggled to penetrate.

The political backdrop further magnified the market’s response. The U.S. administration has made Intel central to its chip sovereignty strategy, with subsidies, CHIPS Act funding, and now direct equity investment.

Trump has also pledged to impose 100% tariffs on imported semiconductors, with exemptions for firms that manufacture in the U.S. By positioning Intel as a “national champion,” Washington has made it clear that the company will not be left to fail, even after years of mounting losses and workforce cuts.

Can Intel sustain the momentum?

The bullish case for Intel rests on its powerful backers, the new strategic partnership, and the scale of investor reappraisal. With Nvidia and the U.S. government on board, Intel suddenly looks like a company with both political protection and commercial relevance.

Analysts at Wedbush Securities called the deal a “game-changer,” arguing it brings Intel “front and centre into the AI game.” CCS Insight described it as a “strategic alignment” that offers Intel a much clearer future. The government’s stake is already up more than 50% on paper in under a month, while Nvidia’s position has gained about $700 million since the purchase.

Nvidia itself gains strategic insurance. By bringing Intel into its ecosystem, it gains a partner in CPUs for data centres and PCs at a time when Chinese bans threaten to dent demand for its GPUs. The partnership also diversifies Nvidia’s exposure away from sole reliance on Arm for CPUs, while giving Intel an opportunity to compete in markets where it has been eclipsed.

If these collaborations deliver tangible results, Intel could build sustained momentum. Investors are already speculating that the stock could extend its rally toward the $40–$45 range if product roadmaps translate into revenue.

The unresolved risks: Intel’s foundry business

Yet, despite the excitement, Intel’s structural problems remain unresolved. Its foundry business, long regarded as key to U.S. chip sovereignty, continues to lose billions of dollars annually. Intel has yet to secure the “significant external customer” it has said is needed to justify continued investment in leading-edge manufacturing. Without this, Intel may abandon its ambitions, leaving the U.S. still reliant on TSMC.

Even Nvidia’s chief executive, Jensen Huang, played down speculation that Nvidia would become a foundry customer. On a press call, he stressed that both firms would “continue to rely on TSMC,” which he described as a “world-class foundry.” This admission highlights the gap between Intel’s geopolitical role and its commercial realities.

The geopolitical environment also adds volatility. Just one day before the Nvidia deal was announced, China’s Cyberspace Administration ordered leading tech firms, including Alibaba and ByteDance, to halt testing and cancel orders for Nvidia’s RTX Pro 6000D chips.

This move escalated the tech trade war and underscored how vulnerable valuations in the sector are to political manoeuvres. For Intel, the risk is that its stock remains more reactive to geopolitics than to company fundamentals.

Intel stock surge and market scenarios

The announcement reshaped the market in a single session. Intel shares surged 22.77% to $30.57, Nvidia rose 3.5%, and Arm fell 4.5% as investors recalibrated future CPU partnerships. The U.S. government’s stake is now worth about $13.3 billion, a $4.4 billion gain in under a month, while Nvidia’s position is worth $5.7 billion, up $700 million since the purchase.

Bullish case

In a bullish scenario, Intel and Nvidia successfully co-develop new products, secure design wins, and Intel stabilises its foundry. In that case, Intel’s stock could build on its rally and sustain higher valuations into 2025.

Bearish case

In a bearish scenario, the collaboration fails to deliver meaningful revenues, Intel’s manufacturing business continues to erode, and the geopolitical tailwinds fade. If so, shares could retrace to the mid-$20s, leaving September’s gap-up as a historic anomaly rather than the start of a new trend.

Intel stock technical outlook

At present, Intel shares are consolidating just above $30 after their sharp rally. The $29.50–$30.00 range is acting as short-term support, showing that buyers are defending gains. However, the candle turning red shows that sell orders are being executed, with profit-taking evident. If the stock fails to hold above $30.55, it could fall back toward the $23.55 or even $19.70 support levels, erasing much of the gap-up and signalling that the move was a temporary repricing rather than a durable rally.

Investment implications

For traders, Intel’s current setup presents short-term opportunities. The $30 support level is critical: holding above it could open upside targets at $34.50 and $40, while a failure could see shares drift back toward $27. Medium-term investors should remain cautious. Intel is being buoyed by political capital and corporate alliances, but its structural weaknesses - especially in its foundry - remain unresolved. For portfolio managers, Intel may be worth holding as a U.S.-backed strategic asset, but until it demonstrates operational progress, it remains a speculative turnaround story rather than a proven leader in the AI era.

Trade the next movements of Intel with a Deriv MT5 account today.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.