Coffee price forecast: Can U.S. trade talks cool a weather-fuelled rally?

Arabica coffee futures remain caught between drought in Brazil and tariffs in Washington. Until either rainfall normalises or a U.S.–Brazil trade deal removes the 50% import duty, prices are likely to stay near multi-month highs. A continued supply squeeze could lift Arabica above $425, while quick diplomatic progress or heavier rains could drag it back toward $380.

Key takeaways

- Brazil’s Minas Gerais drought has cut rainfall to 75 % of normal, the latest in a string of dry years.

- Vietnam’s crop risk from Typhoons Kalmaegi and Fengshen threatens robusta output in the Central Highlands.

- U.S. tariffs on Brazilian coffee have pushed exchange inventories to their lowest since 2024.

- Vietnam logged a record US$8.4 billion in exports, offsetting part of the global shortfall.

- La Niña probability of 71 % points to further dryness through early 2026.

- Global production ≠ ample supply: Arabica deficits persist despite record total output.

Brazil’s drought deepens the arabica deficit

Weather agency Somar Meteorologia reported Minas Gerais - the heart of Brazil’s arabica belt - received just 33 mm of rain in late October, barely three-quarters of the historical average, following a near-dry week earlier. The soil moisture deficit poses a threat to flowering and bean development for the 2026/27 crop.

NOAA’s September update lifted the probability of a La Niña event to 71%, reinforcing expectations of continued dryness across southern Brazil. Conab cut its 2025 arabica estimate by 4.9 % to 35.2 million bags, and total coffee output to 55.2 million bags. Years of sub-par rainfall have already reduced bean size and yields, creating what traders call a “climate premium” in arabica futures.

Trade barriers tighten U.S. supply

In July 2025, Washington imposed a 50 % tariff on Brazilian beans - part of a wider trade confrontation between Presidents Trump and Lula. Brazil supplies roughly a third of America’s unroasted coffee; the duty instantly disrupted shipments.

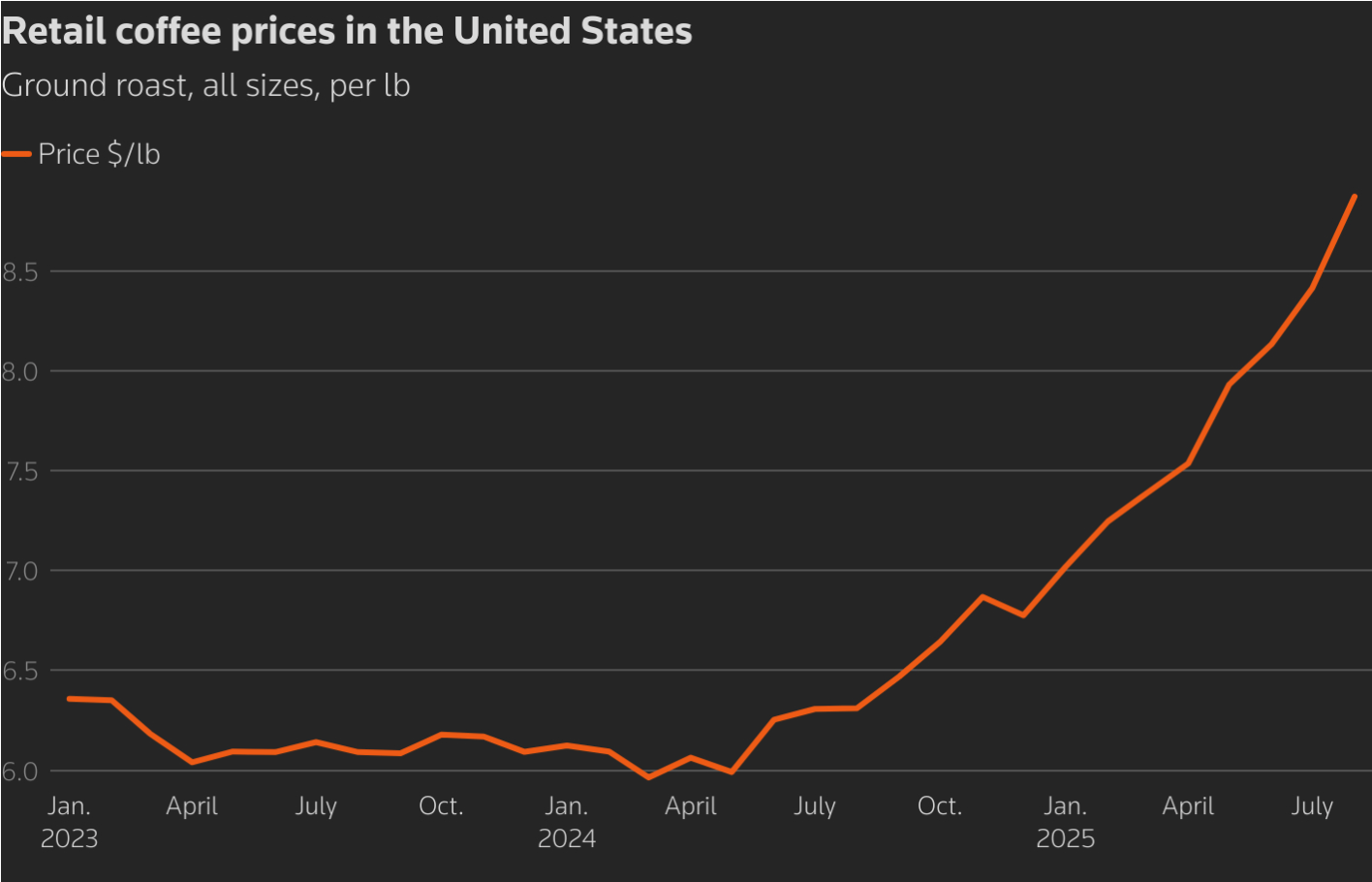

Importers rerouted cargoes to Canada, paid $20–25 per bag cancellation fees, or warehoused beans under bond in Florida to delay tax payment. ICE-monitored arabica stocks have since plummeted to a 1.75-year low of ≈ approximately 431,481 bags, while robusta holdings have declined to ≈ approximately 6,053 lots. Retail coffee prices in U.S. stores rose 41% year-over-year, adding to food inflation.

Both sides now signal progress: Trump described the latest meeting as “positive,” and Lula hinted at a “definitive solution” soon. Any rollback of tariffs would reopen the world’s largest consumer market and relieve U.S. roasters by mid-2026.

Vietnam’s robusta boom - and its limits

Vietnam has been the outlier in 2025’s volatile market. Exports for 2024–25 reached 1.5 million tonnes worth US$8.4 billion, up 55% in value despite minimal volume growth. Average prices jumped 52% to US$5,610 per tonne, reflecting the global supply squeeze.

Europe absorbed 47% of shipments, led by Germany, Italy, and Spain. Farm-gate prices around VND 116,000–118,000 per kg (≈ US$4.6) deliver strong profits, given production costs of VND 35,000–40,000.

However, Typhoons Kalmaegi and Fengshen threaten flooding and landslides in the Central Highlands. Vicofa forecasts a 5–10% increase in 2025/26 output, but warns that persistent storms or fertilizer shortages could reverse those gains. The sector’s new EU “low-risk” status on traceability protects access to European buyers but not against climate volatility.

To explore how traders can capitalise on such volatility, Deriv’s trading calculator help estimate margin and profit scenarios for coffee, gold, and oil positions.

Global production: Record high, but shortages remain

According to the USDA FAS, world coffee production for 2025/26 will reach a record 178.7 million bags (+2.5 %). Yet, arabica output is expected to fall 1.7% to 97 million bags, while robusta rises 7.9% to 81.7 million bags. Ending stocks are expected to rise 4.9% to 22.8 million bags, but this aggregate figure masks an arabica shortfall.

Trader Volcafe projects a global arabica deficit of 8.5 million bags - the fifth straight year of undersupply - wider than last season’s 5.5 million. Even with record totals, the quality mix and logistical bottlenecks leave roasters short of premium beans.

U.S. roasters face an expensive squeeze

American roasters, relying heavily on Brazilian arabica, are drawing down remaining inventories. Some redirected beans to Canada to avoid tariffs, incurring higher freight costs. Others cancelled shipments outright, paying penalty fees.

Small and mid-sized roasters report margins collapsing as replacement beans from Colombia and Mexico cost 10% more, while Brazilian beans - though cheaper - carry the 50% duty.

The ripple effect reaches consumers: a typical supermarket blend has risen from $ 6–7 to $11 per pack. The U.S. Labor Statistics Bureau links these increases directly to reduced imports and weather-related shortages. Analysts expect inventories to fall to 2.5–3 million bags by December, near critical levels.

Coffee price Market outlook

- Bullish scenario: Continued dryness, strong La Niña, and stalled trade talks push arabica through $425, extending the rally into early 2026.

- Base case: Partial tariff relief and modest rains keep prices range-bound $380–$420.

- Bearish scenario: Rapid trade détente plus Vietnam’s larger harvest could pull arabica back to $350–$370 by mid-2026.

Even in the bearish case, structural deficits and climate risks suggest the long-term floor is moving higher.

Coffee price technical analysis

Coffee Arabica prices are consolidating near $411.75, showing a mixed but slightly bullish setup. Bollinger Bands are moderately wide, indicating ongoing volatility. The latest candle is testing the upper mid-band, indicating potential for a short-term push higher if momentum persists.

The key resistance remains at $430.00, where previous rallies faced profit-taking. A decisive break above this could attract fresh buying pressure. On the downside, $390.00 and $378.85 serve as major support zones - a breach below either could trigger liquidation-driven selling.

RSI (14) currently sits around 51, rising sharply from the midline, implying improving bullish momentum but not yet in overbought territory. This reinforces the idea of a cautious recovery phase rather than a breakout trend.

Coffee price investment implications

For traders and investors, the near-term setup points to heightened volatility rather than a sustained correction.

- Short term: Price swings will hinge on U.S.–Brazil trade headlines and rainfall updates; speculative spikes above $425 remain possible.

- Medium-term: Monitor Vietnam’s harvest and La Niña developments, as both could reset the global supply balance.

- Long-term: Structural climate risk keeps the floor higher - arabica below $350 looks unlikely barring a policy breakthrough. Coffee’s current rally may cool, but the underlying heat - political and climatic - shows no sign of dissipating.

For traders seeking exposure, coffee CFDs are available on Deriv MT5, alongside other soft commodities and energy assets, such as gold and oil.

The performance figures quoted are not a guarantee of future performance.