Are global oil prices heading for a $50 price floor?

According to the International Energy Agency (IEA), global oil supply is set to outpace demand growth by a wide margin in 2025 and 2026, raising the prospect of a multi-million barrel per day surplus. Brent crude has already fallen below $66 per barrel, with West Texas Intermediate (WTI) near $62 - levels not seen in over two months.

The combination of record U.S. production, faster-than-expected OPEC+ output increases, and weaker demand forecasts is creating a supply-heavy environment that could push prices towards a $50 per barrel floor unless significant geopolitical disruptions tighten the market.

Key takeaways

- Record U.S. oil output of 21 million bpd in 2025 despite fewer rigs, driven by shale efficiency and technology.

- OPEC+ unwinding cuts early, adding more barrels into the market alongside strong growth from the U.S., Brazil, Canada, and Guyana.

- IEA demand growth forecasts for 2025 and 2026 are less than half OPEC’s, at +0.68m and +0.70m bpd, citing weak consumer confidence.

- A 2026 surplus projection of nearly 3 million bpd - larger than the pandemic-era glut - could pressure prices into the $50s.

- Short-term bullish risks include sanctions on Russia and Iran and Chinese stockpiling for energy security.

- Goldman Sachs base case sees Brent averaging $64 in Q4 2025 and $56 in 2026.

OPEC production increases are overwhelming the market

The IEA’s August 2025 monthly report revised global oil supply growth higher: +2.5 million bpd in 2025 (from +2.1 million) and +1.9 million bpd in 2026.\

This is being driven by two main forces:

- As reported by Reuters, OPEC+ production increases after deciding to unwind recent output cuts faster than planned.

- Non-OPEC growth led by the U.S., Canada, Brazil, and Guyana.

In the U.S., total oil liquids production has seen unprecedented growth. This growth has been achieved with 50% fewer fracking crews than in 2022, thanks to extended-reach drilling, faster well completions, and tapping drilled-but-uncompleted wells (DUCs).

IEA says oil demand growth is slowing

The IEA expects oil demand to grow by just 680,000 bpd in 2025 and 700,000 bpd in 2026 - both 20,000 bpd lower than its prior forecast. Weakness is concentrated in major economies where consumer confidence remains low.

OPEC, however, projects nearly double the demand growth in 2025 at +1.29 million bpd, creating a stark divergence in market outlooks. The IEA’s more conservative stance reflects its assumption of a faster shift to renewables, while OPEC sees continued strong transport fuel demand in emerging markets.

The 2026 glut warning

The IEA projects a potential supply surplus of almost 3 million bpd in 2026, driven mainly by non-OPEC growth. This would surpass the 2020 pandemic-era glut, which sent prices crashing.

Brent’s drop below $66 and WTI’s fall to $62 this week reflect investor concern that even with record refining runs - forecast to reach 85.6 million bpd in August - the market may not absorb the extra crude.

Geopolitics could slow the fall

Political risks remain a wildcard:

- Sanctions on Russia and Iran could restrict output from the world’s third- and fifth-largest producers.

- China’s stockpiling for energy security absorbed surplus barrels earlier this year.

- Trump - Putin - Ukraine talks could introduce further volatility if new measures target Russian exports.

Goldman Sachs sees these factors as potential short-term supports but still expects Brent to average $64 in Q4 2025 before falling to $56 in 2026.

Market impact and price scenarios

If the projected surplus materialises and demand fails to accelerate, Brent could test the $50–$55 range in 2026, according to analysts. However, unexpected supply cuts or geopolitical disruptions could keep prices above $60.

For now, the balance of risk is skewed towards lower prices as supply growth continues to outstrip demand.

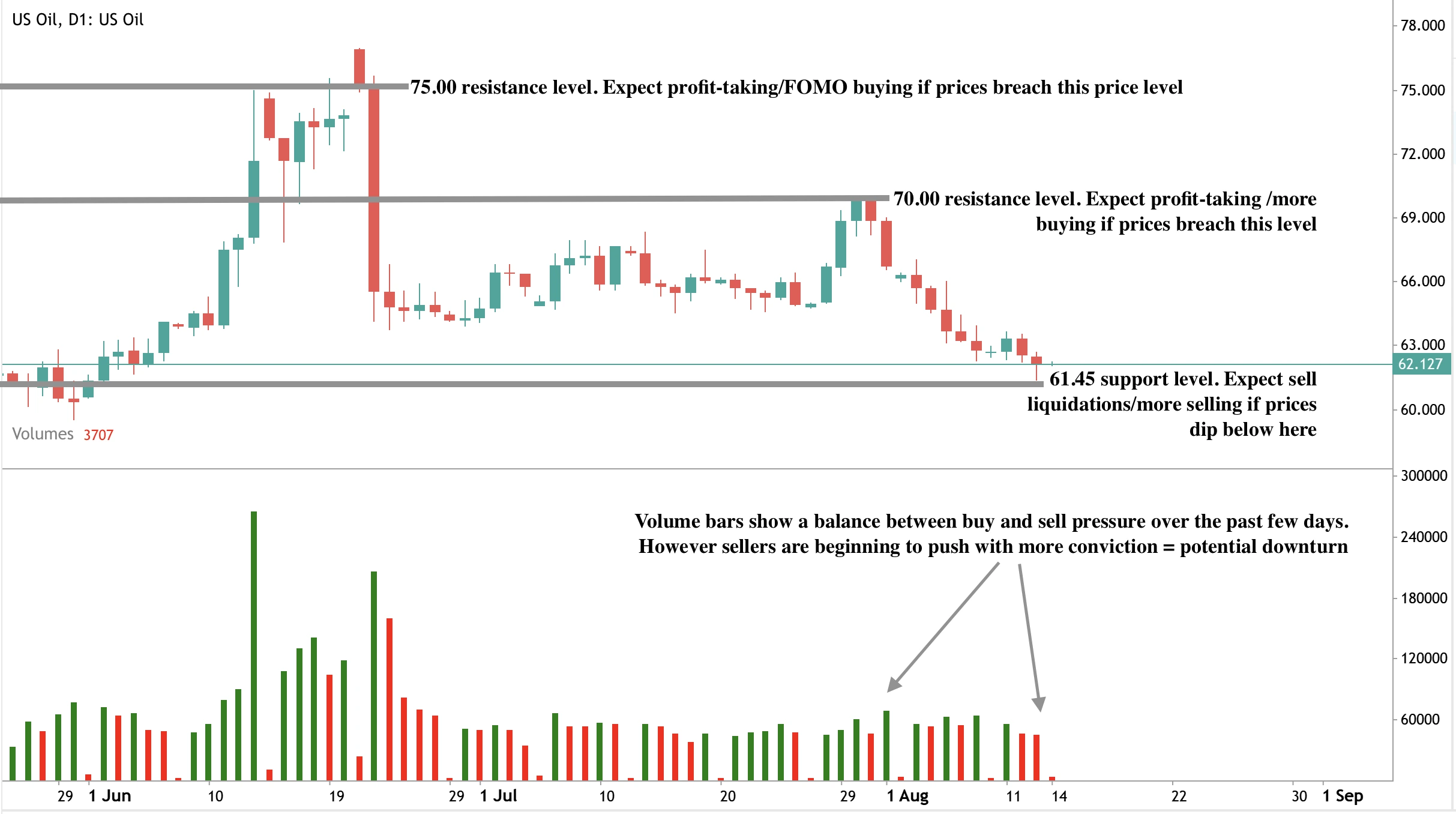

Oil price technical analysis

At the time of writing, oil prices are dipping near a significant support level - hinting that we might see a price rebound if prices touch the $61.45 support level. However, volume bars show that sellers are putting up a spirited fightback against buy pressure - suggesting that we could see a downturn unless buyers pick up momentum. If buyers shrug off the news, prices could see a significant rise with resistance levels at $70.00 and $75.00.

Investment implications

For traders and portfolio managers, the current oil market setup suggests heightened downside risk over the medium term, with a clear bias towards prices moving into the $50–$55 range in 2026 if the projected surplus materialises.

- Short-term strategies may favour tactical buying near strong support levels like $61.45 if geopolitical headlines or sanctions provide temporary price boosts.

- Medium-term positioning should account for the IEA’s bearish demand outlook and the potential for prolonged oversupply, which could keep rallies capped below $70–$75.

- Energy equities tied to U.S. shale and low-cost producers may outperform due to their efficiency and resilience, while higher-cost offshore projects could face margin pressure.

Refining companies could remain profitable given record processing volumes, even if crude prices weaken further.

Trade the next movements of oil with a Deriv MT5 account today.

Frequently asked questions

Why could oil prices fall to $50?

Because global supply is rising nearly four times faster than demand, creating a large surplus that could depress prices into the $50 range.

Which countries are driving supply growth?

The U.S., Canada, Brazil, and Guyana lead non-OPEC growth, while OPEC+ is adding barrels faster than initially planned.

What could prevent a drop to $50?

Sanctions on major producers, Chinese stockpiling, or unexpected demand rebounds could tighten the market and keep prices above $60.

How does refining activity fit into this?

Refining runs are at record highs, but they will not be enough to absorb the projected surplus if the crude supply continues to accelerate.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.