ইয়েনের সম্ভাব্য ক্যারি ট্রেড কি USDJPY উত্থান ঘটাতে পারে?

নোট: আগস্ট ২০২৫ থেকে, আমরা আর Deriv X প্ল্যাটফর্ম অফার করি না।

প্রতিদিন ট্রেডাররা যেন ২০০৬ সালের মতো ইয়েন ক্যারি ট্রেড নিয়ে ফিসফিস করছে, এমনটা শুনতে পাওয়া যায় না। কিন্তু আমরা এখানে এসে পৌঁছেছি। যখন শিরোনামগুলো ট্রাম্পের “ঐতিহাসিক” জাপানের সঙ্গে বাণিজ্য চুক্তির উপর কেন্দ্রীভূত ছিল, চোখ ধাঁধানো সংখ্যাসহ এবং শুল্ক নাটকসহ, FX বাজার ততটা মুগ্ধ নয়। USDJPY ১৪৭ এর নিচে নেমে গেছে, ডলারের গতি কমছে, এবং আসল গল্প হতে পারে এক ধীরে ধীরে ফিরে আসা বিষয়: ক্যারি ট্রেডের প্রত্যাবর্তন।

জাপান এখনও নিম্ন সুদের হার বজায় রেখেছে এবং Fed এখনো পিভট করতে প্রস্তুত নয়, সেই শর্তাবলী যা একসময় ইয়েন ধার করে উচ্চ রিটার্নের জন্য আকর্ষণীয় করেছিল, সেগুলো আবার ধীরে ধীরে ফিরে আসছে।

জাপান-যুক্তরাষ্ট্র বাণিজ্য চুক্তি যা বাজারকে সরাতে চেয়েছিল

প্রেসিডেন্ট ট্রাম্পের মতে, যুক্তরাষ্ট্র জাপানের সঙ্গে “সম্ভবত সবচেয়ে বড় চুক্তি” করেছে। বড় দাবি। চুক্তিতে রয়েছে জাপান থেকে যুক্তরাষ্ট্রে প্রায় ৫৫০ বিলিয়ন ডলারের বিনিয়োগ – যা বন্ড রিটার্নের চেয়ে বেশি চোখ কপালে তুলেছে – এবং যুক্তরাষ্ট্রে প্রবেশ করা জাপানি পণ্যের উপর ১৫% পারস্পরিক শুল্ক। এর বিনিময়ে, জাপান তার সুপরিচিত সুরক্ষিত বাজার যুক্তরাষ্ট্রের গাড়ি, ট্রাক এবং এমনকি চালের জন্য খুলে দিয়েছে।

জাপানের শীর্ষ বাণিজ্য আলোচক, রিওসে আকাজাওয়া, X-এ “মিশন সম্পন্ন” পোস্ট করেছেন। কিন্তু বাজার প্রায়ই কোনো প্রতিক্রিয়া দেখায়নি। USDJPY আসলে নেমে গেছে, এবং ডলার সূচক নরম হয়েছে।

রাজনৈতিক নাটকের সবকিছুর মাঝেও, ট্রেডাররা ওয়াশিংটন থেকে শিরোনামগুলো থেকে বেশি মনোযোগ দিয়েছে সুদের হার প্রত্যাশা এবং ঝুঁকি গতিবিধিতে।

ক্যারি ট্রেড কী, এবং এখন কেন গুরুত্বপূর্ণ?

আপনি কি কখনও ক্যারি ট্রেড সম্পর্কে শুনেছেন? এটি আবার ফিরে আসছে, এবং এখন কেন এটি গুরুত্বপূর্ণ তা এখানে। মূলত, এটি সস্তায় ধার নিয়ে অন্যত্র উচ্চ রিটার্নের সম্পদে বিনিয়োগ করার ব্যাপার। বছরের পর বছর ধরে, জাপানের প্রায় শূন্য সুদের হার পরিবেশ এটিকে প্রধান ফান্ডিং কারেন্সি করে তুলেছিল।

এটি ২০০৮ সালের পর ফ্যাশন থেকে বেরিয়ে গিয়েছিল, QE বছরগুলিতে সাময়িকভাবে ফিরে এসেছিল, এবং তারপর আবার অদৃশ্য হয়ে গিয়েছিল যখন অস্থিরতা ফিরে এসেছিল এবং বিশ্বব্যাপী রিটার্ন সমান হয়ে গিয়েছিল।

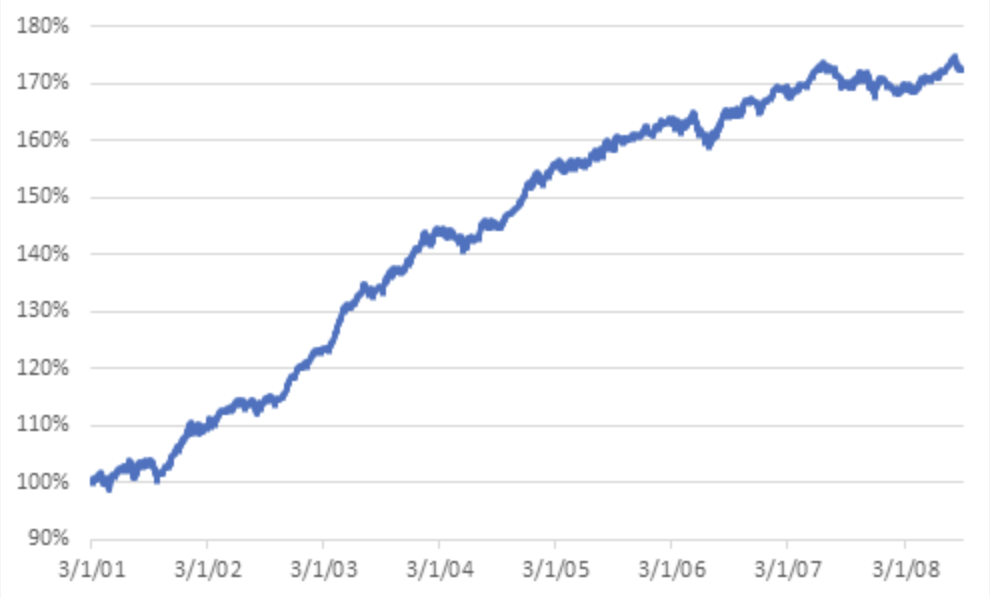

নিচে আর্থিক সংকটের আগে ক্যারি ট্রেডের সামগ্রিক রিটার্ন দেখানো হয়েছে।

এবং নিচে আর্থিক সংকটের পর ক্যারি ট্রেডের সামগ্রিক রিটার্ন দেখা যাচ্ছে।

কিন্তু এখন, কিছু পরিবর্তন হচ্ছে। Fed হয়তো এখনও তার পূর্বাভাসে সুদের হার কমানোর কথা বলছে, কিন্তু স্থায়ী মুদ্রাস্ফীতি এবং শুল্ক-চালিত মূল্য চাপ এটিকে সতর্ক রাখছে। অন্যদিকে, জাপান, ধীরগতির বৃদ্ধি, দুর্বল মজুরি তথ্য এবং নাজুক রাজনৈতিক পটভূমি নিয়ে, সংকোচনের জন্য খুব কম সুযোগ রাখে। এটি সেই ধরনের সুদের হার পার্থক্য তৈরি করে যা ক্যারি ট্রেডাররা পছন্দ করে।

USDJPY ঠিকই পালিয়ে যাচ্ছে না

এই সবের পরেও, USDJPY উড়ে যাচ্ছে না। বরং উল্টো। জুটি সম্প্রতি ১৪৭.০০ স্তরের নিচে নেমে গেছে, গতি সূচকগুলো ক্লান্তির সংকেত দিচ্ছে। এটি বছরের শুরুতে সুদের হার পার্থক্য এবং ঝুঁকি-অনুভূতির ঢেউয়ের উপর চড়েছিল। কিন্তু এখন? ট্রেডাররা বিরতি নিচ্ছে।

এর একটি কারণ হল BoJ বিশ্বব্যাপী সংকোচনের পরেও সাইডলাইনেই রয়েছে। বিশ্লেষকরা বলছেন জাপানের নরম মুদ্রাস্ফীতি তথ্য এবং রাজনৈতিক অস্থিরতা নীতিনির্ধারকদের সতর্ক রাখছে। এর সাথে যুক্ত করুন জাপান কি সত্যিই যুক্তরাষ্ট্রের অর্থনীতিতে ৫৫০ বিলিয়ন ডলার প্রবাহিত করতে পারবে কিনা সেই অনিশ্চয়তাও, এবং আপনি পাবেন এমন একটি বাজার যা আগ্রহী, কিন্তু নিশ্চিত নয়।

রাজনীতি ও নীতি টোকিওতে মিলিত হচ্ছে

জাপানের অভ্যন্তরীণ পটভূমি ভুলে যাবেন না। প্রধানমন্ত্রী শিগেরু ইশিবার দল সম্প্রতি তিন আসনে উচ্চকক্ষের সংখ্যাগরিষ্ঠতা হারিয়েছে। তিনি ছোট ছোট জোট অংশীদারদের সমর্থনে টিকে আছেন, কিন্তু তার দখল দুর্বল, এবং তা গুরুত্বপূর্ণ।

কম সংখ্যাগরিষ্ঠতা অর্থনৈতিক সংস্কারে কম সুযোগ দেয়, বিশেষ করে যদি যুক্তরাষ্ট্রের দাবি বাড়ে। তবুও, বাজার ফলাফলকে বেশ গ্রহণ করেছে, কারণ তারা ইশিবাকে ভালোবাসে না, বরং এটি একটি সম্ভাব্য বাজার-কম্পিত বিরোধী দলের উচ্চ করের ঝুঁকি থেকে রক্ষা করে। আপাতত, BoJ-এর নৌকা না ডুবানোর কারণ আরও বেড়েছে।

একটি ফিসফিস, এখনও গর্জন নয়

তাহলে ইয়েন ক্যারি ট্রেড কি ফিরে এসেছে? পুরোপুরি নয়। কিন্তু যেসব শর্ত এটি লালন করেছিল - কম অস্থিরতা, সুদের হার পার্থক্য, এবং একটি নীরব BoJ - সেগুলো আবার ফিরে আসছে। USDJPY জুটি হয়তো এখনো বড় ধরনের ব্রেকআউট করছে না, কিন্তু এটি আর শুধু শিরোনামের উপর ভিত্তি করে ট্রেড হচ্ছে না।

ইয়েনের জন্য নিরাপদ আশ্রয়ের চাহিদা কমছে, বিশেষ করে বাণিজ্য চুক্তি ১ আগস্টের শুল্ক সময়সীমাকে নিরপেক্ষ করে দিয়েছে। যদিও জাপানের বিনিয়োগের পরিমাণ হয়তো বাস্তবের চেয়ে বেশি, বিশ্লেষকরা বলছেন কাঠামোগত গল্প - পার্থক্যপূর্ণ কেন্দ্রীয় ব্যাংক এবং পুরনো কৌশলগুলোর ধীরে ধীরে ফিরে আসা - তা যথেষ্ট গুরুত্ব বহন করে।

ক্যারি ট্রেড চিৎকার করে না। যখন কেউ দেখছে না তখন চুপিচুপি ফিরে আসে। ট্রেডাররা হয়তো এখনও ট্রাম্পের শুল্ক কৌশল বা জাপানের বিনিয়োগ প্রতিশ্রুতির বিশ্বাসযোগ্যতা নিয়ে বিতর্ক করছে, কিন্তু পটভূমিতে ইয়েন ধীরে ধীরে তার পুরনো ভূমিকা খুঁজে পাচ্ছে - আশ্রয় হিসেবে নয়, বরং ফান্ডিং টুল হিসেবে।

আর যদি সেই গতি বাড়ে? USDJPY হয়তো শোনাতে শুরু করবে।

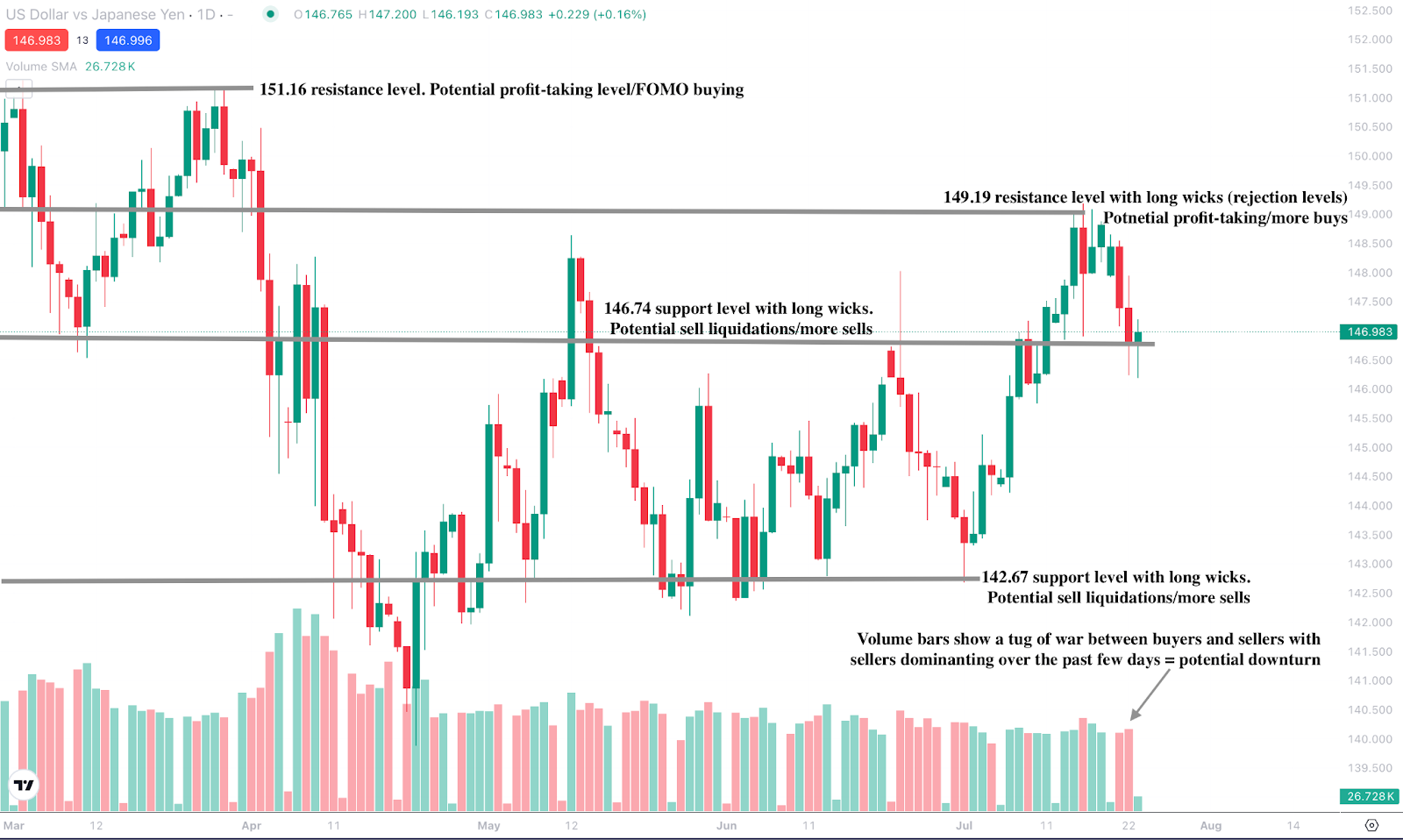

USDJPY প্রযুক্তিগত দৃষ্টিভঙ্গি

লিখার সময়, জুটি পূর্বের পতন থেকে কিছুটা পুনরুদ্ধার করেছে, একটি সমর্থন স্তরের আশেপাশে অবস্থান করছে, যা উপরের দিকে সম্ভাব্য গতি নির্দেশ করে।

তবে, ভলিউম বারগুলো গত দুই দিনে শক্তিশালী বিক্রয় চাপ দেখাচ্ছে, ক্রেতাদের থেকে খুব কম প্রতিরোধ পাওয়া যাচ্ছে, যা ইঙ্গিত দেয় যে যদি ক্রেতারা দৃঢ়তার সাথে চাপ না দেয় তবে আরও পতন হতে পারে। নিচে গিয়ে $146.74 এবং $142.67 সমর্থন স্তরে থামতে পারে। বিপরীতে, উপরে উঠলে $149.19 এবং $151.16 মূল্য স্তরে প্রতিরোধ পেতে পারে।

আজই Deriv MT5 অ্যাকাউন্ট দিয়ে USDJPY এর গতিবিধি ট্রেড করুন।

অস্বীকৃতি:

উল্লেখিত পারফরম্যান্স সংখ্যা ভবিষ্যতের পারফরম্যান্সের গ্যারান্টি নয়।