Will gold central bank buying sustain its rally as dollar reliance fades?

Yes, central bank demand is a powerful force shaping gold’s long-term trajectory, as countries diversify reserves away from the US dollar and reinforce a trend of de-dollarization. This steady official-sector buying provides a strong foundation for prices, acting as a safety net even in volatile conditions. At the same time, the short-term outlook hinges on shifting variables — from Federal Reserve policy decisions and dollar strength to broader geopolitical tensions — which will determine whether gold can push above the critical $3,450 resistance or remain capped below it.

Key takeaways

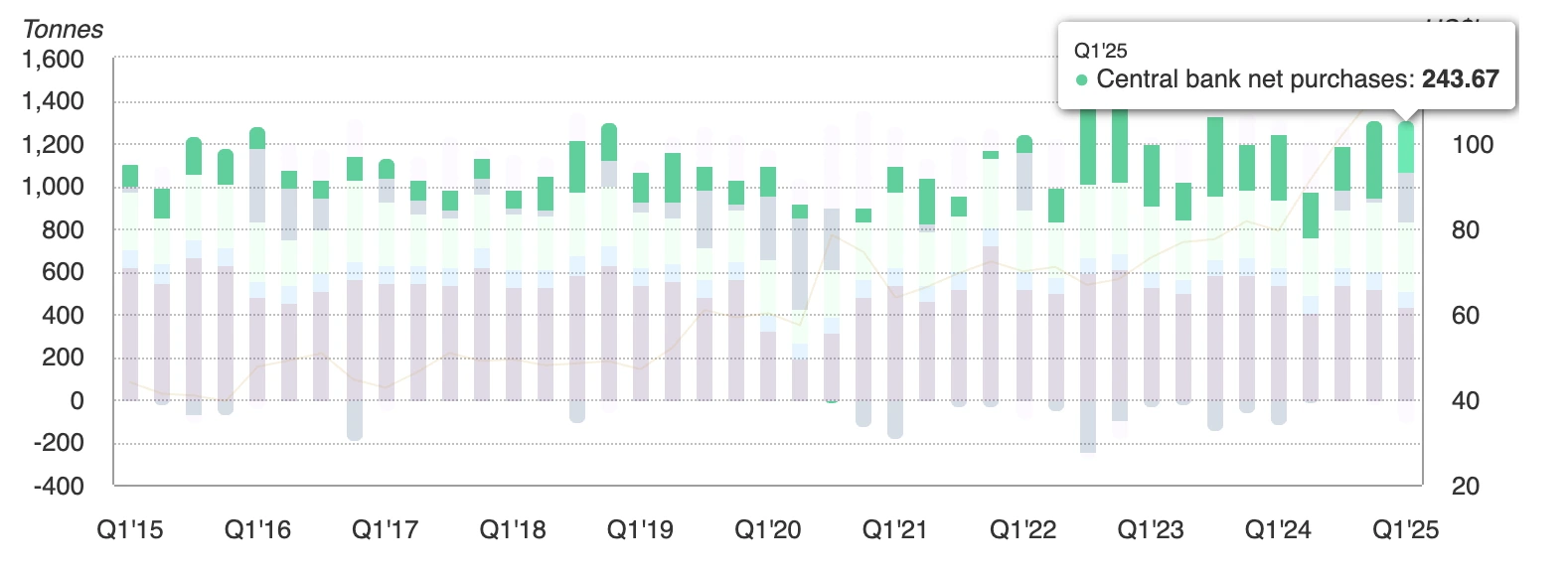

- Foreign central banks now hold more gold than US Treasuries, the first time since the 1990s.

- Global official sector gold demand hit 244 metric tons in Q1 2025, far above the five-year average.

- Gold-backed ETFs attracted $38 billion in inflows in H1 2025, after $15 billion of outflows in 2024.

- Retail buying in India and China is surging as households shift savings into gold.

- ASEAN and BRICS are formalising local-currency trade settlement systems to reduce dollar use.

- The dollar’s reserve share has slipped below 47%, while gold’s share is climbing toward 20%.

- Fed independence concerns and high September rate-cut odds are further boosting demand for non-yielding assets.

Gold central bank buying and its return as a reserve anchor

The latest World Gold Council data shows central banks bought 244 tons of gold in the first quarter of 2025, the strongest Q1 in years.

Gold now accounts for nearly one-quarter of total annual inflows, the highest proportion since the late 1960s.

This shift isn’t confined to one region. Purchases are geographically broad - from China and India to the Middle East and Latin America - underscoring how central banks are rebalancing away from dollar-denominated assets. The seizure of Russia’s reserves in 2022 accelerated this rethink, highlighting the political risk embedded in holding Treasuries.

De-dollarization trend moves from rhetoric to policy

For years, de-dollarization was a buzzword. In 2025, it has become policy.

ASEAN’s 2026–30 Strategic Plan prioritises local-currency trade settlement for goods and investment. Analysts at Bank of America estimate this could cut dollar invoicing in the bloc by 15% within five years.

BRICS economies are also expanding their cross-border payment networks, including currency-swap agreements and settlement platforms that bypass the dollar.

These initiatives are reinforced by political factors such as Trump’s protectionist stance is unnerving trading partners, while the weaponisation of dollar assets - sanctions and reserve seizures - has pushed policymakers to diversify faster.

Academic research suggests that once the perceived cost of holding dollars rises above a threshold, diversification becomes self-reinforcing. That threshold may be in sight soon with some analysts predicting that the dollar’s reserve share may drop below 50% within the next decade - down from more than 70% at the start of the century.

Gold ETF inflows renaissance as trust shifts

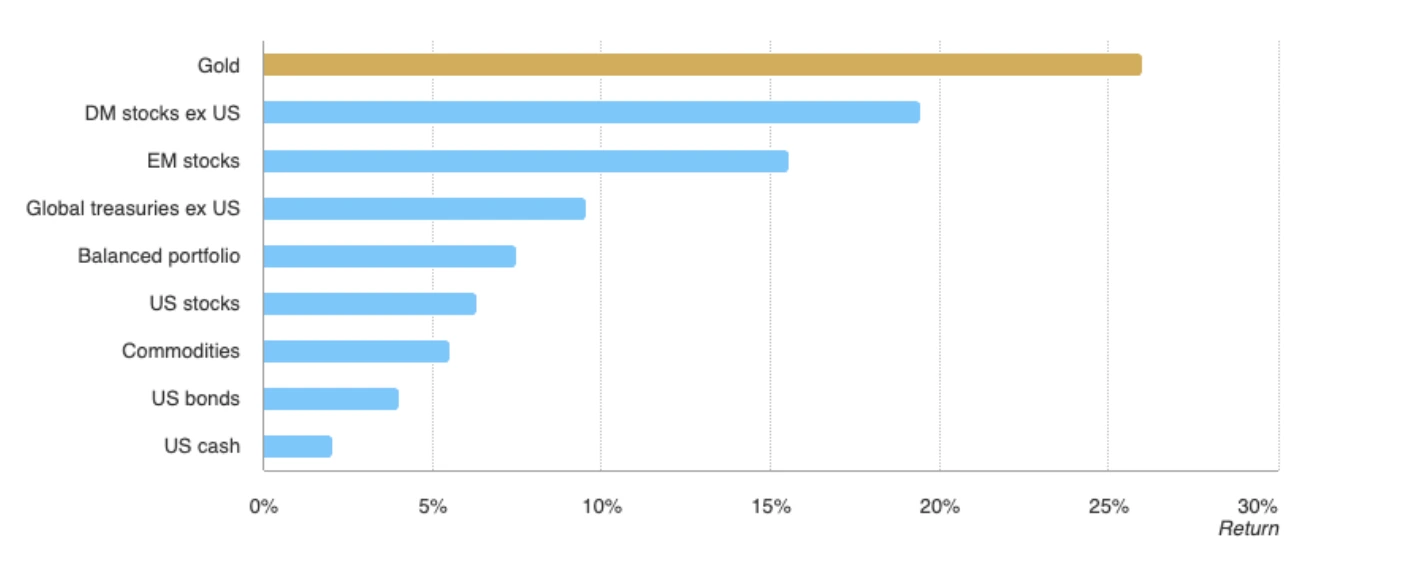

Gold has outperformed the MSCI World Index and the Bloomberg Aggregate Bond Index in 2025, as well as major global asset classes, extending its role beyond a dollar hedge to a foundation of global trust.

After two sluggish years, global gold ETFs saw inflows of nearly $38 billion in H1 2025, equivalent to 322 tons, marking the strongest start to a year since 2020. Indian and Chinese households are also buying physical gold at record levels, viewing it as a reliable store of value as local currencies face volatility.

If this trend spreads beyond Asia, spot prices could push past $3,400 toward $3,450 and beyond. Meanwhile, the traditional inverse relationship between gold and the Dollar Index continues to hold, with dollar weakness reinforcing bullion’s strength.

Fed politics add fuel to the rally

The gold rally is also being fed by political instability in Washington. President Trump’s attempt to fire Fed Governor Lisa Cook sparked a legal standoff that raised fresh doubts about the independence of the Federal Reserve.

Markets are now pricing in an 85% probability of a September rate cut, up from 84.7% a week earlier, according to CME FedWatch.

Chair Powell has acknowledged some labour market cooling, though he remains cautious on the inflation impact of Trump’s policies.

Lower interest rates reduce the opportunity cost of holding gold, reinforcing central bank and retail demand. Meanwhile, the dollar has retreated on weaker rate expectations, further boosting bullion.

Gold at $3,400 - momentum or exhaustion

Gold’s resilience around the $3,400 level has created a pivotal moment. The outlook splits into two clear paths:

- Bullish drivers

- Central bank and ETF demand is structural, not cyclical.

- De-dollarization policies are anchoring long-term flows.

- September Fed rate cut bets remain high, lowering the opportunity cost of holding gold.

- Central bank and ETF demand is structural, not cyclical.

- Bearish risks

- US GDP expanded 3.3% in Q2 2025, showing economic resilience.

- Inflation remains above target, which may slow or cap Fed easing.

- A stronger dollar rebound could stall momentum below $3,450 resistance.

- US GDP expanded 3.3% in Q2 2025, showing economic resilience.

Gold technical insights

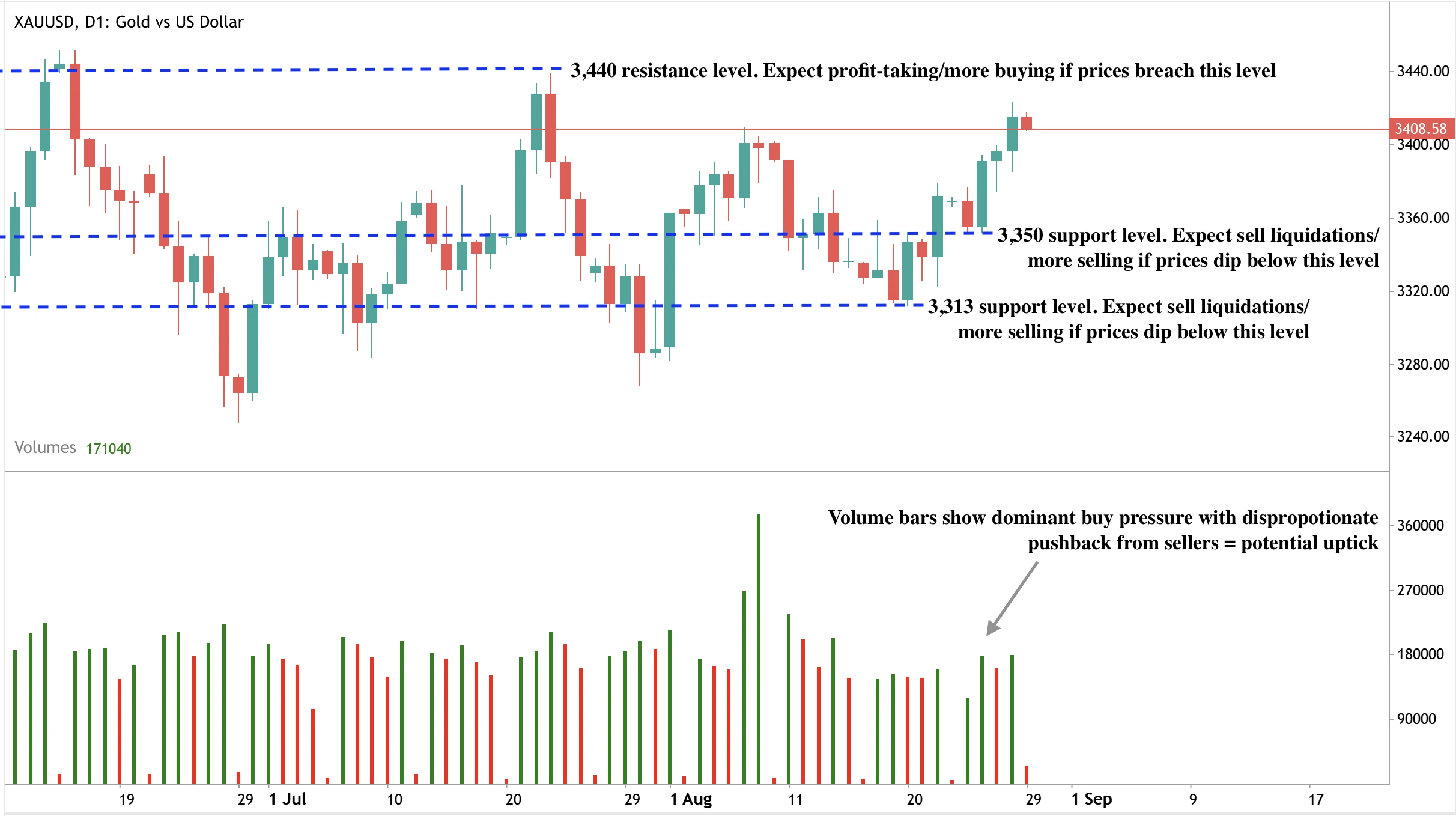

At the time of writing, gold has retreated from its monthly high rally close to a resistance level - hinting at potential reversal. However, the volume bars show dominant buy pressure with little pushback from sellers, suggesting a potential further leg up. If prices extend higher, they may face resistance at the $3,440 level. Conversely, if momentum fades, gold could find support at $3,350 and $3,313, which now form key floors for traders to watch.

Market outlook and price scenarios

If central bank and ETF demand remain firm, a break above $3,450 could trigger a new wave of technical buying, opening the path toward record highs. Conversely, if the Fed holds back on easing or inflation remains sticky, gold may consolidate below resistance and risk a pullback.

Either way, the balance of risks favours stronger long-term prices. The structural decline in dollar dominance is not a short-term trade, but a reordering of the reserve system — with gold back at the centre.

Investment implications

For investors, gold remains a portfolio diversifier rather than an all-in bet. Its role is strengthening as central banks reshape their reserves and as policymakers pursue de-dollarization strategies. In the short term, traders will watch the $3,450 level as a pivot point. In the long term, the erosion of dollar primacy suggests gold’s renaissance is far from over.

Frequently asked questions

Why are central banks buying more gold than US Treasuries?

Because Treasuries now carry both market and political risks. The 2022 seizure of Russia’s reserves showed the vulnerability of dollar assets, while gold offers neutrality, liquidity, and no counterparty risk. This makes it a more reliable anchor for reserves.

Can gold break above $3,450?

Yes, but it depends on alignment between central bank demand and Fed policy. Strong ETF inflows and Asian retail buying already support prices, and a September rate cut could be the catalyst for a clean breakout.

What risks could stall the rally?

Upside momentum could be capped if US growth stays firm, inflation proves sticky, or the dollar rebounds. Any of these would make it harder for gold to sustain levels above $3,450.

Is gold replacing the dollar as the world’s reserve asset?

Not yet - the dollar still dominates global reserves. But its share has slipped below 47% while gold is nearing 20%, showing a clear shift toward diversification. Gold is becoming a complement, not a replacement.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.