Swap-free weekends on Synthetic Indices

Deriv’s swap-free weekend lets traders hold Synthetic Index positions from Friday to Monday without paying overnight funding. The pause removes two days of financing while markets stay open 24/7, improving cost efficiency and strategy consistency across Deriv MT5 (Standard and Zero-spread).

It helps traders reduce costs while maintaining active strategies during continuous Synthetic Index trading.

This guide explains how the swap-free weekend works, why it matters in today’s CFD landscape, and how Deriv traders can use it to refine weekend strategies.

Quick summary

- Meaning: Weekend pause in overnight funding from the last Friday rollover to the first Monday rollover.

- Value: Synthetic Indices trade continuously; the pause cuts carry costs without interrupting strategies.

- How it works: Covers all Synthetic Indices on Deriv MT5 automatically.

- Effect: Better back-test parity, lower drag on expectancy, and uninterrupted automation.

Weekend funding used to be a predictable cost line for 24/7 markets. By removing it, Deriv gives active traders a small but consistent efficiency gain that compounds over time.

What is a swap-free weekend, and how does it work?

A swap (also known as overnight funding or rollover) is the financing adjustment applied to leveraged CFD positions held past the broker’s daily cut-off. During Deriv’s swap-free weekend, the accrual pauses from Friday’s final rollover to Monday’s first.

In practice:

- Pause starts: After the Friday 21:59 GMT rollover each week.

- Resumes: At the Monday 21:59 GMT rollover.

- Applies to: All long and short Synthetic Index trades on Deriv MT5.

Any positions open between Friday 21:59 GMT and Monday 21:59 GMT are held swap-free.

CFD funding reflects the cost of leverage: a principle defined by regulators such as the FCA and ESMA. The weekend pause simply suspends that cost, keeping statements transparent while reducing total charges.

For traders running automated systems or grid strategies, the absence of weekend swaps prevents performance distortions between live and back-tested data.

Why are Deriv synthetic indices ideal for swap-free weekends?

Synthetic Indices operate continuously and are unaffected by macroeconomic events or real-world news. This stability makes them ideal for around-the-clock strategies.

The swap-free window enables traders to hold weekend positions without incurring funding drag while maintaining their exposure.

This is especially beneficial for swing, grid, and algorithmic trading on Deriv, where uninterrupted data flow and price consistency are crucial for reliable automation and optimisation.

Deriv’s Synthetic Indices also come in distinct volatility families, from Vol 10 to Vol 250, enabling traders to choose exposure suited to their risk appetite. The swap-free pause ensures all of these remain efficient to hold through weekends.

How do swap-free weekends interact with leverage and margin?

Leverage and margin determine how efficiently traders deploy capital. During the swap-free window, equity remains stable since no financing is deducted, which improves compounding and frees up margin for tactical adjustments.

For instance, a trader using 1:500 leverage on a USD 10,000 notional position saves the equivalent of two days’ funding each weekend. Over months, these small gains support better capital retention and smoother equity curves.

Maintaining a free-margin buffer of 300–500% is advisable, ensuring that weekend volatility in 24/7 markets never threatens open positions.

Harolyn Medina Calderon, Risk Specialist at Deriv, elaborates:

“Maintaining a strong free margin during the weekend window remains essential. It ensures traders aren’t penalised for holding when Synthetic Indices stay open 24/7.”

How do swap-free weekends connect within Deriv’s ecosystem?

Since synthetic indices trade 24/7, Deriv MT5 can maintain uninterrupted automation for users.

The feature integrates Deriv’s entire trading infrastructure into a cost-efficient ecosystem that combines pricing, risk management, and transparency.

Table 1 – Deriv swap-free weekend ecosystem overview

Together, these relationships make swap-free weekends a transparent, 24/7 cost solution within Deriv’s ecosystem.

How do swap-free weekends affect CFD funding costs?

The primary advantage is that CFD funding costs are eliminated for two full days. Traders still experience price movement and margin variation, but no interest accrues.

Table 2 – Trading behaviour comparison: with swaps vs swap-free weekends

Most brokers apply daily or “triple-swap” adjustments mid-week; Deriv’s approach removes weekend accrual entirely, creating a cost-efficient structure for Synthetic Indices.

What are the benefits of weekend trading strategies?

Weekend traders can maintain open positions, automation, and analytics without funding erosion.

For weekend trading strategies, such as trend-following or grid systems, the pause improves back-test alignment and stabilizes compounded results.

It also enables strategy developers to run weekend tests continuously without compensating for variable financing inputs, enhancing model reliability.

What benefits do Deriv MT5 users gain?

- Markets covered: All Synthetic Indices (Volatility, Crash/Boom, Step, Jump, and more).

- Platforms: Deriv MT5 (Standard, Zero-spread).

- Conditions: No swaps accrue during the weekend; spreads, margin, and execution remain normal.

- Not an Islamic account: The pause is time-based, not eligibility-based.

- Platform details:

- Deriv MT5: “Swap” fields show 0.00 over weekends; statements confirm no funding.

The platform thereby maintain identical weekend conditions, giving quants and discretionary traders full consistency across systems.

“For most traders, the weekend swap pause is invisible — yet it directly improves strategy accuracy,” explains Muhammad Hamza Akram, Deriv Platform Product Manager.

“Automation tools on Deriv MT5 perform closer to theoretical models because there’s no overnight cost distortion.”

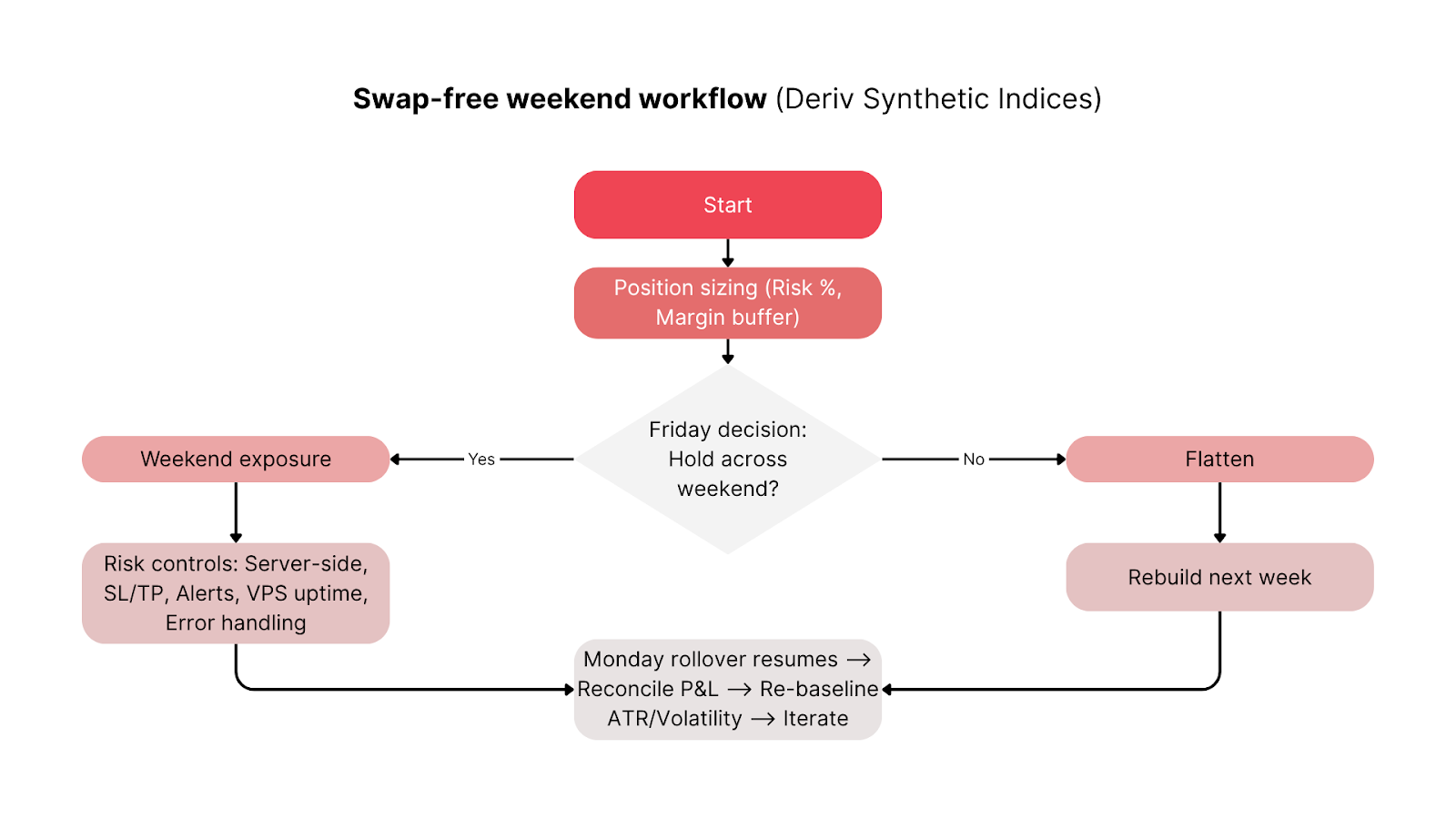

How can traders integrate swap-free weekends into their workflow?

To benefit fully, align capital, execution, and monitoring routines with Deriv’s weekend window.

Pre-Friday checklist:

- Maintain a free margin of 300–500% to absorb variance.

- Place server-side stops and limits.

- Confirm VPS stability and alert timings for automated strategies.

- Diversify index exposure (e.g., combine Vol 25 with Vol 75).

During the weekend:

- Monitor positions periodically; prices move 24/7 even without swaps.

- Avoid manual intervention unless volatility spikes.

Monday reconciliation:

- Verify no weekend funding entries in statements.

- Adjust stops or scaling if volatility changes after the Monday roll.

This simple routine turns a passive weekend into a controlled, data-driven trading window.

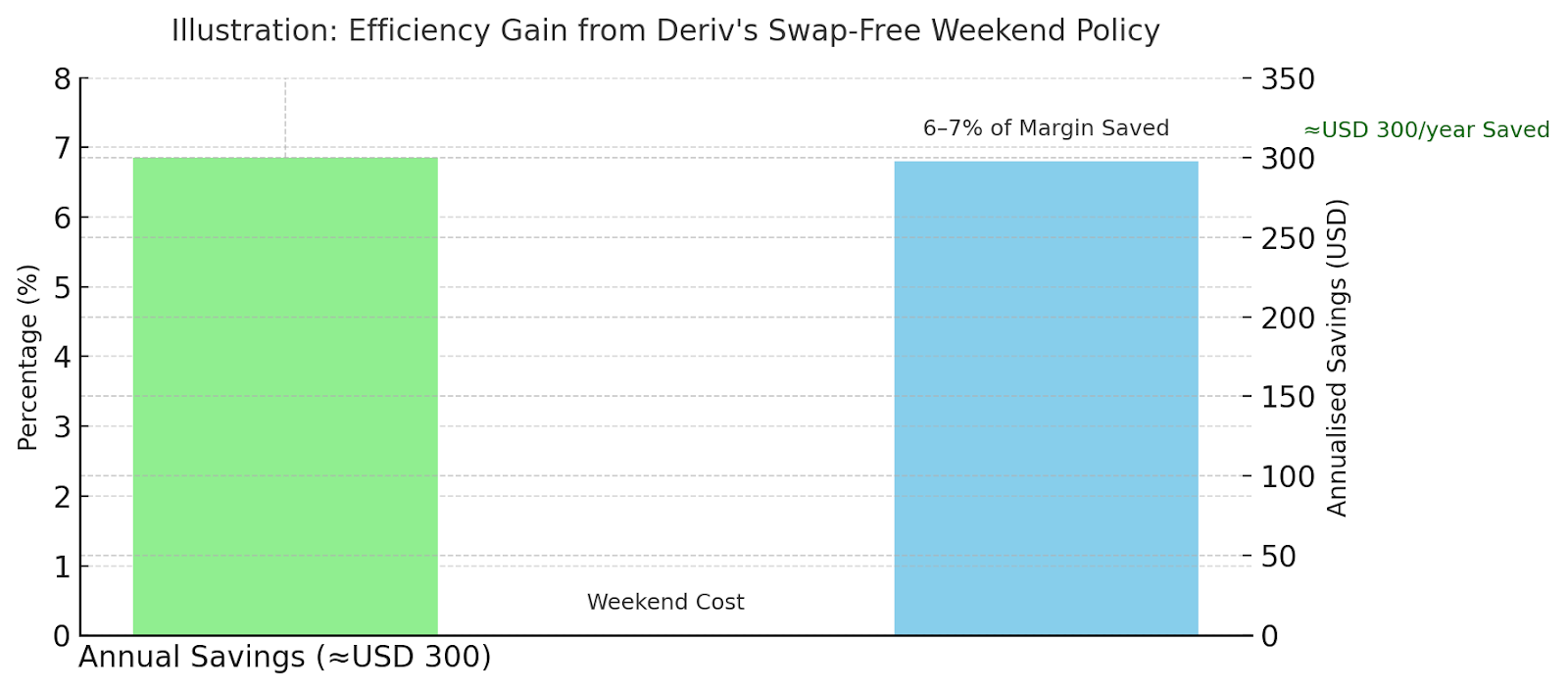

How much can traders save each year?

Assume a 2.5% annualised funding rate. Two weekend days equal roughly 0.014% of notional.

At 1:500 leverage, that’s about 6–7% of the posted margin saved each weekend. Over a year, frequent weekend positions can reduce total funding by hundreds of USD.

For example:

- Scenario A: USD 20,000 notional swing position → ≈ USD 120 annual savings.

- Scenario B: automated grid of USD 50,000 aggregate notional → ≈ USD 300 saving.

These differences compound for active systems trading 40–45 weekends per year.

“Weekend funding has always been a small but compounding cost for leveraged traders,” says Alassana Kane, Senior Trading Analyst at Deriv.

He goes on: “By removing this element for Synthetic Indices, we give traders more predictable performance metrics and closer alignment between live data and algorithmic testing results.”

How do other brokers handle weekend swaps under FCA and ESMA rules?

Most brokers apply rollover charges continuously, whereas Deriv uniquely removes them across the weekend window.

Table 3 – Broker weekend policy comparison

This policy complies with FCA and ESMA rules on cost transparency and client protection, ensuring that weekend financing is clearly disclosed and applied fairly.

Deriv Compliance team, Rose Tanya, mentions:

“The swap-free weekend aligns perfectly with global CFD cost-disclosure standards. It reflects our broader commitment to transparency under FCA and ESMA supervision.”

How does Deriv’s swap-free weekends redefine 24/7 trading?

Deriv’s swap-free weekend policy transforms how traders manage exposure on Synthetic Indices. It lowers CFD funding costs, supports continuous automation on Deriv MT5, and complies with FCA and ESMA transparency standards.

For traders aiming to refine weekend trading strategies or optimise leverage and margin use, this feature offers measurable efficiency without additional complexity.

So if you’re wondering how to lower weekend trading costs on Synthetic Indices, Deriv’s swap-free feature gives you that flexibility automatically.

It reduces CFD funding costs, supports continuous automation, and aligns fully with regulatory best practice, which is a clear edge for Deriv traders in 2025 and beyond.

Disclaimer:

This content is not intended for EU residents. The information contained within this blog article is for educational purposes only and is not intended as financial or investment advice. The information may become outdated. No representation or warranty is given as to the accuracy or completeness of this information. We recommend you do your own research before making any trading decisions.