Results for

The hard asset question for 2026: Why Platinum is in focus

Hard assets are no longer behaving like a niche hedge. In 2025, gold pushed decisively into record territory, silver surged nearly 150%, and platinum rose more than 120% - a scale of movement that signals something deeper than a short-lived flight to safety.

Hard assets are no longer behaving like a niche hedge. In 2025, gold pushed decisively into record territory, silver surged nearly 150%, and platinum rose more than 120% - a scale of movement that signals something deeper than a short-lived flight to safety, according to analysts. At the same time, traditional defensive assets such as the US dollar and long-dated Treasuries have struggled to perform when geopolitical risk flares.

As investors look beyond the initial rush into gold and silver, attention is shifting toward what comes next. With supply constraints tightening, strategic classifications changing, and geopolitics increasingly shaping commodity markets, platinum is emerging as a serious question for 2026 rather than a forgotten footnote.

What’s driving the hard-asset shift?

The renewed US–Europe standoff over Greenland has reinforced demand for precious metals, but it did not create it. Gold and silver were already rallying before geopolitical tensions resurfaced, driven by rising concerns over fiscal discipline, monetary credibility, and institutional reliability in the United States. Long-end Treasury yields climbing during risk events have become a recurring signal that confidence, not growth, is being questioned.

This environment has exposed a critical vulnerability in portfolio construction. Assets that depend on government promises - currencies and sovereign bonds - are no longer providing consistent protection when uncertainty rises. As a result, capital has flowed toward assets that lie entirely outside the financial system. Gold benefits first in these moments, but history shows that once the hard-asset theme takes hold, it tends to broaden.

Why it matters

What distinguishes this cycle from previous risk episodes is the erosion of trust in traditional safe havens, according to analysts. The dollar and the yen have struggled to attract the defensive flows they once did, while US Treasuries have reacted to geopolitical stress with higher yields rather than lower ones.

Markets appear increasingly sensitive to the scale of US deficits and the perception that monetary policy could face political pressure in the coming years.

Analysts have begun to frame the move into hard assets as structural rather than tactical. Ole Hansen of Saxo Bank has argued that metals are now responding to “system-level doubt rather than headline-driven fear”. In that context, diversification within the hard-asset space becomes as important as initial exposure, which helps explain why attention is expanding beyond gold.

Impact on the metals market

Gold remains the anchor, according to analysts, but silver’s outsized rally has started to raise questions. At current levels, silver risks triggering a collapse in industrial demand, particularly in price-sensitive sectors. That does not invalidate the bullish case, but it does complicate it, encouraging investors to reassess relative value within precious metals rather than adding indiscriminately.

Platinum stands out in this reassessment. Despite its strong performance in 2025, it remains well below its historical highs and has lagged gold over the past several years. More importantly, its supply-and-demand dynamics look increasingly fragile. Unlike gold, platinum is both an investment asset and a critical industrial input, making it more sensitive to shifts in manufacturing, regulation, and geopolitics.

Platinum’s supply constraints and industrial reality

Roughly 42% of platinum demand still comes from the automotive sector, where it is used in catalytic converters. For years, expectations of rapid electric vehicle adoption weighed heavily on prices. Those assumptions are now being revised. TD Securities expects internal combustion engine demand, especially in the US, to remain more resilient than previously forecast, offering continued support for platinum and palladium.

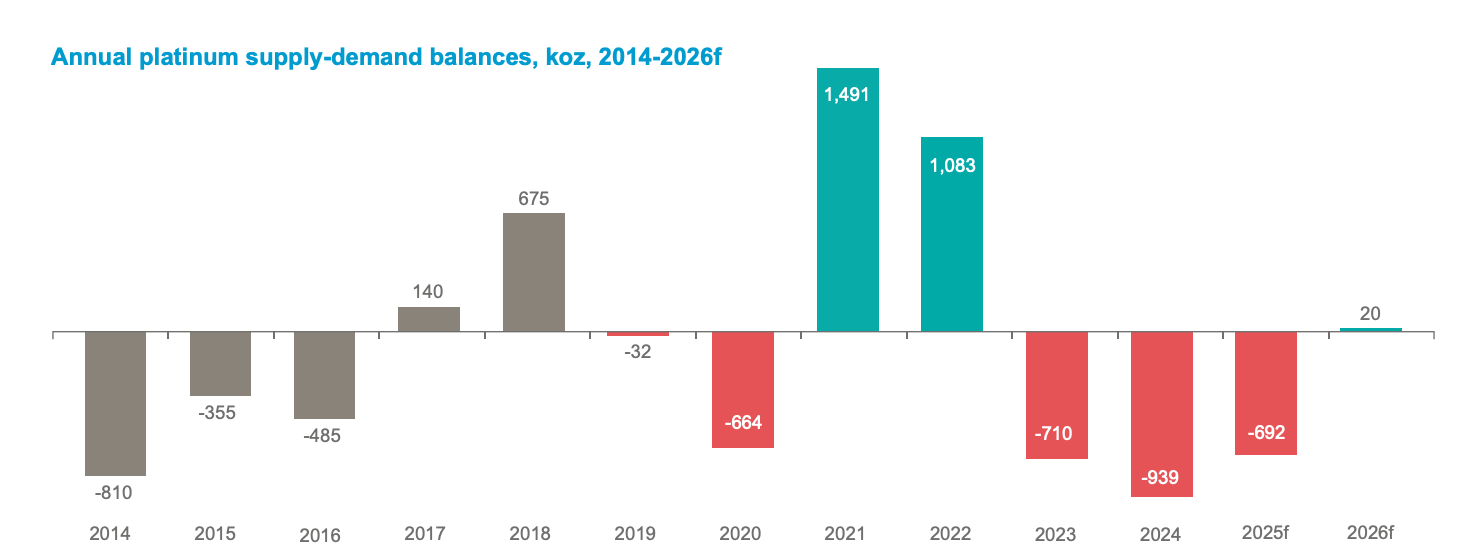

At the same time, supply is tightening. The World Platinum Investment Council reported that above-ground inventories now cover only about 5 months of demand, after 3 consecutive years of deficits.

Limited investment in new mining projects has capped production growth, leaving the market exposed to shocks. According to Nicky Shiels of MKS PAMP, the sector faces “persistent structural deficits” rather than temporary imbalances.

Geopolitics, critical metals, and strategic stockpiling

Platinum’s outlook has also been reshaped by politics. In November 2025, the US Geological Survey classified platinum and palladium as critical metals, elevating their strategic importance. That designation has intensified discussions around supply security, trade policy, and inventory management at both corporate and state levels.

The possibility of US tariffs under an ongoing Section 232 investigation, even if delayed, has reinforced a shift toward “just-in-case” stockpiling. In physical markets such as London, this has contributed to an artificial tightness, as material is withheld from circulation. In a world where strategic resources are increasingly treated as national assets, price formation is no longer purely an economic process.

Expert outlook for 2026

Forecasts for platinum in 2026 reflect this tension between opportunity and risk. MKS PAMP sees prices potentially reaching $2,000 per ounce, while TD Securities expects averages closer to $1,800 in the second half of the year. At the more cautious end, BMO Capital Markets projects prices around $1,375, arguing that any oversupply could ease pressure on spot markets.

What unites these views is uncertainty around inventories. WPIC scenarios suggest that continued exchange inflows could deepen deficits, while sustained outflows might even push the market into surplus by 2026. That sensitivity underscores why platinum is increasingly viewed as a strategic question rather than a simple continuation of the gold trade.

Key takeaway

The hard-asset rally is no longer just about gold. It reflects a deeper shift in how investors view risk, trust, and diversification. As silver tests levels that strain industrial demand, platinum is moving into focus as a metal shaped by supply tightness, strategic importance, and geopolitical risk. For 2026, the critical signals to watch will be inventories, trade policy, and whether investor demand expands beyond gold into the broader precious metals complex.

Platinum technical outlook

Platinum remains elevated following a sharp upside acceleration, with price consolidating near recent highs while trading along the upper Bollinger Band. The sustained width of the bands reflects persistently high volatility, even as the pace of the advance has slowed.

Momentum indicators show a moderation rather than a reversal, with the RSI dipping back toward the midline after previously reaching stretched levels. From a structural perspective, the broader move remains intact above the $2,200 area, while earlier breakout zones near $1,650 and $1,500 sit well below current prices, underscoring the magnitude of the recent advance. Overall, current price action reflects a pause near highs within a still-elevated volatility regime.

Why Gold and Silver are exploding higher on Trump’s Greenland gambit

Gold and Silver surged to fresh record highs in early Asian trading as markets digested a dramatic escalation in geopolitical risk from Washington.

Gold and Silver surged to fresh record highs in early Asian trading as markets digested a dramatic escalation in geopolitical risk from Washington. US President Donald Trump’s announcement of sweeping tariffs on European allies over Greenland jolted investors, triggering a rush into safe-haven assets and unsettling global equities.

The moves had little to do with inflation or rate cuts. Instead, it reflects growing unease over trade fragmentation, diplomatic breakdowns, and the weaponisation of tariffs as a form of geopolitical leverage. As tensions spill across the Atlantic, gold and silver are once again behaving like political barometers rather than inflation hedges.

What’s driving Gold and Silver higher?

The immediate catalyst for gold’s explosive move is Trump’s threat to impose 10% tariffs from 1 February, rising to 25% by June, on eight European countries unless the US is allowed to purchase Greenland. The nations targeted include Germany, France, Denmark, the UK, Sweden, Norway, Finland, and the Netherlands - all long-standing US allies.

Markets reacted not just to the tariffs themselves, but to the precedent they set. Linking trade policy directly to territorial demands represents a sharp escalation in economic coercion. Investors quickly priced in the risk of retaliation, policy paralysis, and prolonged uncertainty, conditions under which gold historically thrives. European officials warned that the move risks a “dangerous downward spiral” in transatlantic relations, reinforcing the sense that diplomacy may struggle to contain the fallout.

Silver has followed gold higher, though with more volatility. While gold benefits almost immediately from fear-driven flows, silver’s response reflects a mix of safe-haven demand and concern over industrial disruption.

With European leaders openly discussing retaliatory measures on as much as €93 billion of US goods, fears of fractured supply chains and slower manufacturing activity are beginning to underpin silver prices as well.

Why it matters

This rally matters because it signals a shift in the drivers of precious metals. Recent gold strength has persisted despite strong US labour market data and fading expectations of near-term Federal Reserve rate cuts. Futures markets now price the next Fed easing no earlier than June, yet gold continues to push higher.

That divergence highlights a deeper concern. Investors are no longer focused solely on interest rates or inflation trajectories. Instead, they are reacting to political risk that cannot be easily modelled or hedged.

As Saxo Markets’ chief investment strategist, Charu Chanana, put it, the key question is whether this moves “from rhetoric to policy”, because once deadlines are set, markets must treat the threat as real.

Impact on markets, trade, and investors

The broader market reaction has been swift. European and US equity futures fell, while the US dollar weakened against the euro, sterling, and yen. That softer dollar removed a traditional headwind for gold, amplifying its upside momentum.

Importantly, this is occurring even as US bond yields remain elevated, reinforcing that the move is driven by risk aversion rather than monetary easing.

Silver’s role is more complex. If trade tensions escalate without tipping the global economy into recession, silver could outperform gold due to tighter supply conditions and its exposure to strategic industries. However, should tariffs meaningfully slow industrial output, silver may face sharper pullbacks on negative growth headlines. That dual exposure explains the increased volatility now visible in silver markets.

For investors, the message is clear. Precious metals are once again being treated as portfolio insurance. ETF inflows and derivatives positioning suggest institutional demand is accelerating, even as physical consumption remains secondary. The focus is on capital preservation, not jewellery or industrial usage.

Expert outlook

Looking ahead, the near-term trajectory for gold hinges on whether Trump’s tariff threats are implemented or diluted through negotiation. 1 February has become a critical date for markets. Confirmation of policy action could push gold deeper into uncharted territory, with some bank analysts already outlining scenarios above $4,800 per ounce if retaliation follows.

Silver’s outlook depends on how trade tensions intersect with economic resilience. Persistent geopolitical stress combined with steady growth would favour silver on a relative basis. A sharp deterioration in trade flows, however, would likely see gold widen its lead. Investors are also watching EU discussions around activating the bloc’s anti-coercion instrument, a rarely used tool that could significantly escalate the dispute.

Key takeaway

Gold’s record-breaking surge is a response to political shock, not economic weakness. Trump’s Greenland-linked tariff threats have revived trade war fears and pushed investors toward hard assets. Silver is participating, though with greater sensitivity to growth risks. Whether this rally extends now depends on one question: will these threats translate into policy, or will diplomacy regain control?

Silver technical outlook

Silver has surged to around $93, marking a near-38.7% gain in just 30 days, with trading volume estimated at roughly 15 times normal levels - one of the most aggressive silver rallies seen in decades. The move places silver firmly in price-extension territory, with technical conditions more commonly associated with late-stage or blow-off phases. Gold has also pushed sharply higher, reinforcing the broader precious-metals momentum backdrop.

Trend strength remains undeniable. ADX readings near 52 point to a very strong, mature trend, while momentum indicators are stretched across timeframes: RSI is above 70 on the daily chart, near 86 on the weekly, and above 90 on the monthly. This combination reflects powerful upside momentum, but also highlights growing exhaustion risk as the rally matures.

Price continues to track along the upper Bollinger Band with expanding volatility - a classic parabolic profile. At the same time, the nearest structurally meaningful support sits near $73, more than 20% below current levels, underscoring just how stretched the move has become. Historically, when ADX reaches these extremes, any loss of momentum tends to be followed by sharp, fast pullbacks rather than shallow consolidations.

Gold technical outlook

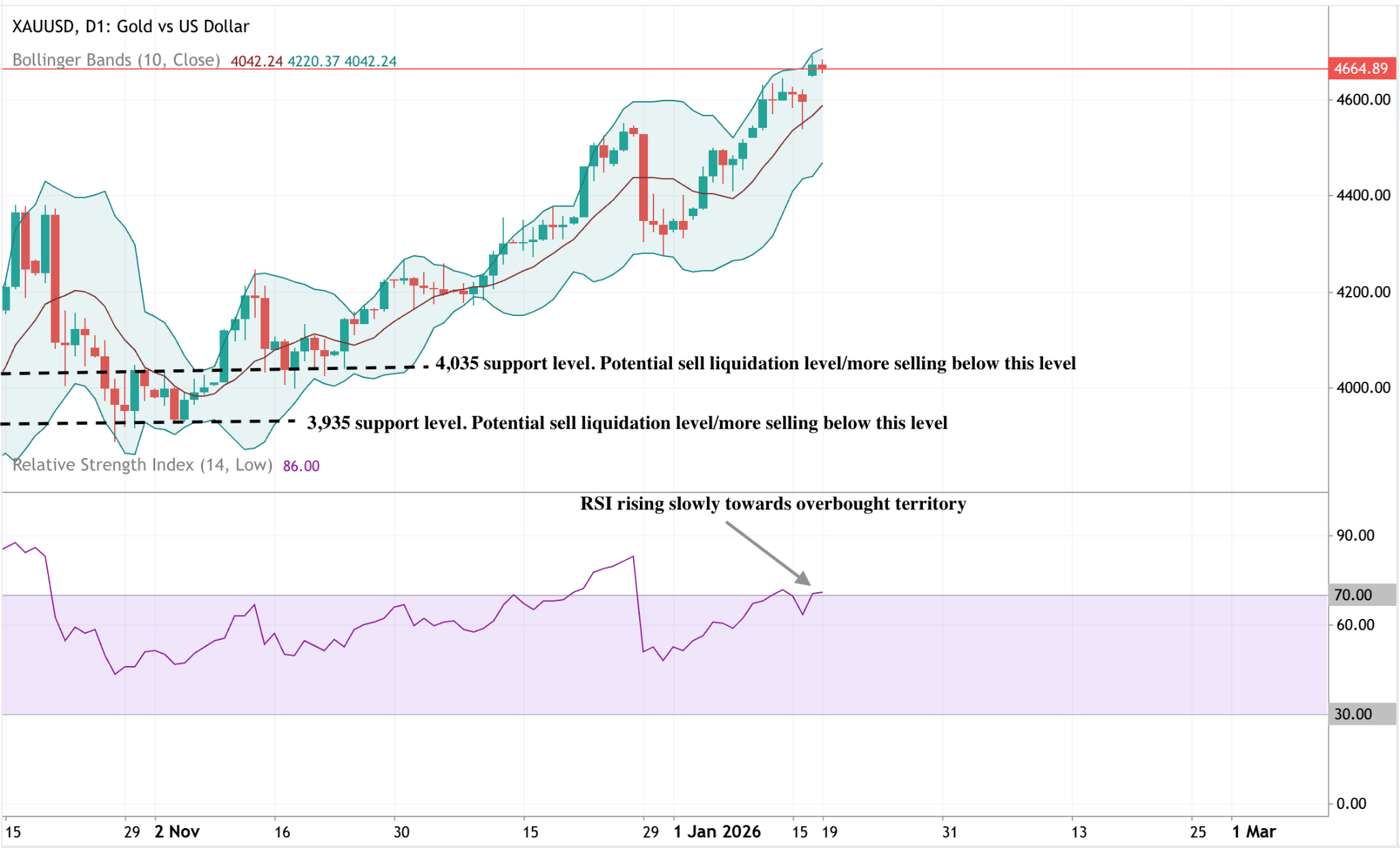

Gold continues to trade near recent highs after a strong upside extension, with price pressing against the upper Bollinger Band - a sign of sustained bullish momentum but also elevated short-term stretch. Volatility remains expanded, reflecting strong participation rather than a low-conviction drift.

Momentum indicators show similar conditions: the RSI is rising gradually toward overbought territory, suggesting momentum is firm but no longer accelerating aggressively. Structurally, the broader trend remains intact, while price holds above the $4,035 and $3,935 zones, with recent price action pointing to consolidation rather than an immediate trend reversal.

Why Silver is falling after hitting an all-time high

Silver is falling because the conditions that drove it to record highs have shifted, analysts say. The move marked a decisive pause in one of the strongest rallies seen across the commodities market this year.

Silver is falling because the conditions that drove it to record highs have shifted. After surging to an all-time peak near $93.90 earlier in the week, spot silver retreated more than 2% during Friday’s Asian session, trading around $90.40 an ounce.. The move marked a decisive pause in one of the strongest rallies seen across the commodities market this year.

The pullback reflects a combination of easing trade-related supply fears, delayed expectations for US interest rate cuts, and a cooling in geopolitical risk. Together, these factors have stripped away the short-term premium that fuelled silver’s surge, even as longer-term structural demand remains intact.

What’s driving Silver?

The most immediate catalyst behind silver’s decline was a shift in US trade policy. President Donald Trump ordered US trade officials to enter negotiations with key partners rather than impose immediate tariffs on imports of critical minerals. That decision directly removed a supply-side risk that had been aggressively priced into silver earlier in the week.

Silver’s reaction highlights its dual role in global markets. As both a precious metal and a key industrial input used in electronics, renewable energy, and advanced manufacturing, silver is acutely sensitive to supply-chain expectations. When tariff risks faded, the scarcity premium embedded in prices unwound quickly, prompting a wave of profit-taking after the metal’s run to record highs.

Why it matters

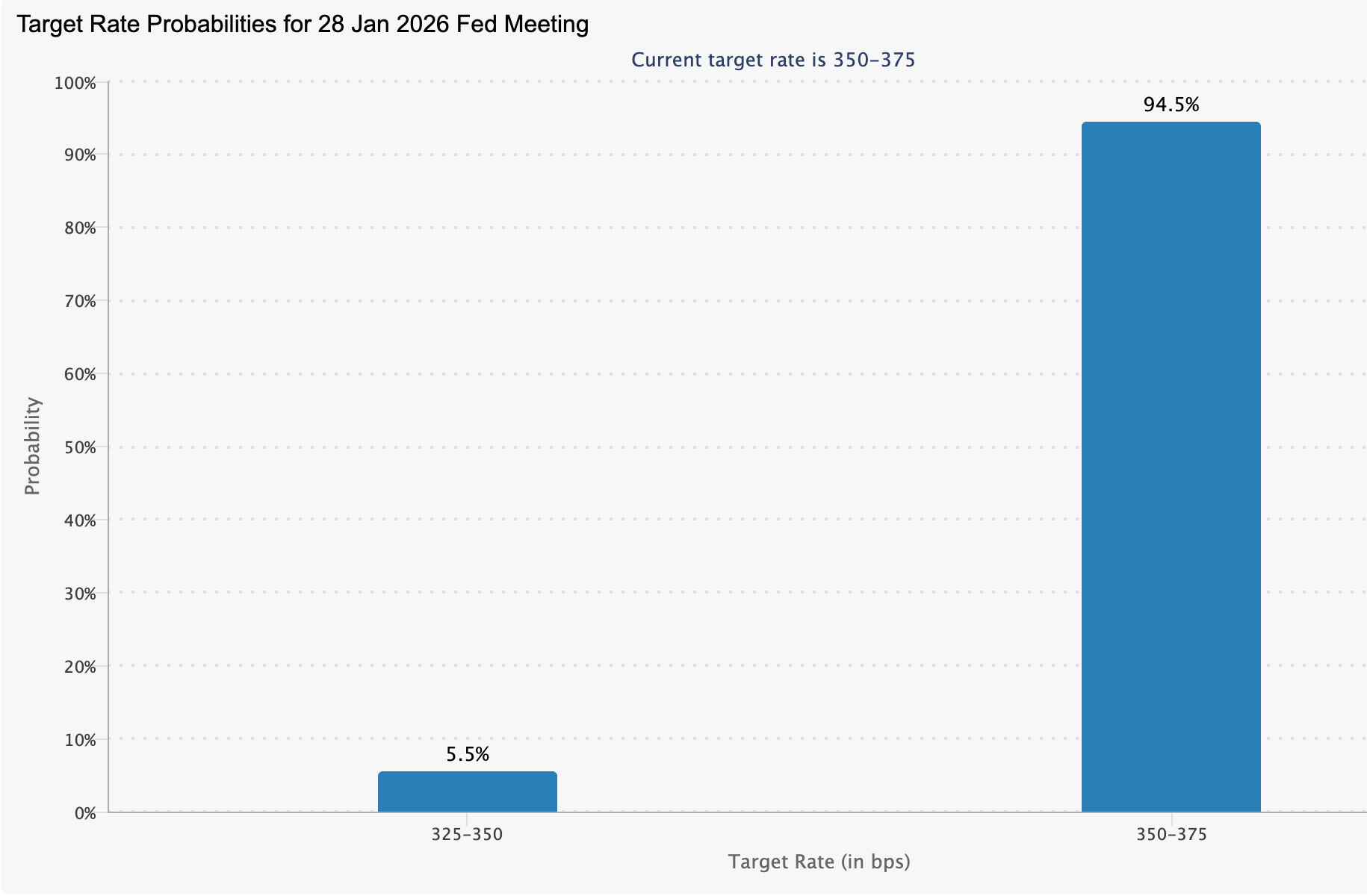

Monetary policy has added a second layer of pressure. Markets are now almost fully priced for the Federal Reserve to hold interest rates steady at its January meeting, with CME FedWatch indicating roughly a 95% probability of no change.

Expectations for the first rate cut have been pushed back to June as inflation data remains sticky.

That backdrop weighs on silver’s near-term appeal. As a non-yielding asset, it becomes less attractive when interest rates stay elevated, and the US dollar strengthens.

Rahul Kalantri, Vice-President of Commodities at Mehta Equities, noted that recent US macroeconomic data has lifted the dollar to multi-week highs, creating headwinds for bullion prices despite strong underlying demand.

Impact on precious metals markets

Silver’s retreat has echoed across the broader precious metals complex. Gold futures for February delivery fell 0.55% to $4,611 an ounce, while spot gold slipped to around $4,604.52. Platinum and palladium also moved lower, reflecting broad-based profit-taking rather than isolated weakness in silver.

Geopolitical sentiment has also played a role. President Trump’s less confrontational tone on Iran reduced immediate safe-haven demand, improving risk appetite across equity markets. Asian stock indices traded mostly higher, tracking Wall Street’s positive tone, while gold extended losses toward $4,590 as defensive positioning unwound. Silver, which often tracks gold during shifts in risk sentiment, followed suit.

Expert outlook

Despite the short-term correction, silver’s fundamentals remain supportive in the long term. The US has openly acknowledged that it lacks sufficient domestic capacity to meet demand for critical minerals, reinforcing silver’s strategic role across multiple industries. That structural backdrop continues to underpin longer-term optimism, even as prices digest recent gains.

For now, silver appears firmly driven by macro signals. Federal Reserve communication, movements in the US dollar, and any renewed geopolitical tension will likely determine whether the metal stabilises or extends its correction. Until clearer signals emerge, consolidation below recent highs looks more probable than a decisive trend reversal.

Key takeaway

Silver is falling because the short-term forces that pushed it to record highs have shifted. Easing tariff risks, delayed rate-cut expectations, and improving risk sentiment have reduced the immediate price premium. Even so, strong industrial demand and strategic relevance continue to underpin the broader trend. The next decisive move will depend on macro policy signals and global risk dynamics.

Technical perspective: Momentum beneath the pullback

From a technical perspective, silver continues to display unusually strong momentum beneath the surface of the pullback.

Daily momentum indicators are elevated, with the 14-day relative strength index hovering around 70.7, a level commonly associated with overbought conditions following sharp rallies.

Trend strength remains notable. The average directional index stands at 51.18, a historically high reading that reflects an exceptionally strong directional move rather than a loss of underlying momentum.

.jpg)

Could Nvidia's 'DRIVE' breakthrough spell doom for Tesla?

Nvidia’s DRIVE platform won't erase Tesla’s data lead, but it lowers the barriers to entry for full autonomy across the market.

In short, no, according to analysts, but it does weaken one of Tesla’s most powerful investment narratives.

Nvidia’s expanded DRIVE platform does not suddenly make Tesla irrelevant in autonomous driving, nor does it erase years of proprietary data and software development. What it does do is lower the barriers to entry for full autonomy, giving rival carmakers faster and cheaper access to self-driving tools that once looked uniquely difficult to replicate.

That distinction matters because Tesla’s valuation increasingly rests on future autonomy rather than current vehicle sales, which fell 8.5% in 2025. Nvidia’s CES 2026 announcement reframes the debate: autonomy may still define the future of transport, but it no longer looks like a single-winner race. For investors, the question is shifting from whether autonomy arrives to who monetises it first.

What’s driving Nvidia’s push into autonomous driving?

Nvidia’s move into autonomous systems is not a distraction from its core business. It is a deliberate expansion of artificial intelligence beyond data centres and into physical environments, where machines must interpret uncertainty in real-time.

In fiscal 2025, Nvidia generated $115.2 billion in data center revenue, primarily from AI infrastructure, which provided the scale and capital to invest heavily in applied autonomy. At CES 2026, Nvidia unveiled a major upgrade to its DRIVE platform centred on the Alpamayo family of models. Unlike earlier autonomous systems that relied mainly on pattern recognition, Alpamayo focuses on reasoning-based decision-making.

That shift targets one of the industry’s most challenging problems: rare, unpredictable “long tail” events that often compromise safety. By combining large, open datasets with simulation tools such as AlpaSim, Nvidia aims to shorten development timelines for manufacturers that lack Tesla’s decade-long data advantage.

Why it matters for Tesla’s autonomy narrative

Tesla’s investment case has gradually pivoted away from cars and towards software-led autonomy. Despite declining vehicle sales, Tesla shares pushed to new highs in 2025 as investors factored in the future value of the Cybercab robotaxi and autonomous ride-hailing services. Ark Invest has projected $756 billion in annual revenue from robotaxis by 2029, a figure that dwarfs Tesla’s current revenue base.

The problem is timing. Tesla’s Cybercab is not expected to enter mass production until April 2026, and its Full Self-Driving software remains unapproved for unsupervised use in the United States. Any delay in regulatory clearance risks widening the gap between expectation and execution. Nvidia’s announcement does not block Tesla’s path, but it makes that path more crowded at precisely the moment investors are least tolerant of slippage.

Impact on the autonomous vehicle market

Nvidia’s expanded DRIVE ecosystem strengthens a broad field of competitors. Global carmakers, including Toyota, Mercedes-Benz, Volvo, Hyundai, Jaguar Land Rover, and others, already rely on Nvidia's hardware and software to accelerate their autonomous vehicle programs. The addition of reasoning-based AI tools reduces development costs and compresses timelines, allowing established manufacturers to challenge Tesla’s perceived lead.

Meanwhile, Alphabet’s Waymo continues to widen its operational advantage. Waymo now completes more than 450,000 paid autonomous ride-hailing trips each week across five US cities, generating real-world data and regulatory credibility that few rivals can match. When Tesla’s Cybercab enters service, it will not be pioneering a new market, but rather attempting to catch up in one that is already established.

Expert outlook: hype versus execution

The market reaction to Nvidia’s CES announcement was swift, with some investors interpreting it as a pivotal moment for autonomous driving. Morgan Stanley, however, urged caution. The bank argued that new tools do not automatically translate into commercial dominance, instead pointing to integration, validation, and cost control as the true differentiators.

Analyst Andrew Percoco noted that autonomy remains a multi-year execution challenge, not a single product cycle. Nvidia may supply the picks and shovels, but manufacturers must still prove safety at scale and secure regulatory approval. The decisive phase begins in 2026, when Nvidia’s partners attempt deployment, and Tesla seeks to move from promise to paid service.

Key takeaway

Nvidia’s DRIVE expansion does not spell doom for Tesla, but it does undermine the idea that autonomy is Tesla’s exclusive prize. By lowering the cost and complexity of self-driving development, Nvidia is reshaping the competitive landscape at a critical moment. The next year will determine whether Tesla can convert vision into revenue before rivals close the gap. For markets, execution now matters more than ambition.

Tesla technical outlook

Tesla is consolidating below the $495 level after a sharp rejection from recent highs, with price drifting back toward the middle of its recent range. Bollinger Bands are beginning to contract after a period of expansion, signalling a slowdown in volatility following the earlier directional move. This aligns with momentum conditions stabilising rather than accelerating.

The RSI is hovering around the midline, reflecting a neutral momentum profile after the prior upswing cooled. Overall, price action suggests a pause within a broader range rather than a renewed directional push, with market participants reassessing momentum after the failed upside extension. These technical conditions can be monitored in real time using advanced charting tools on Deriv MT5, where traders can analyse price action, volatility, and momentum across global markets.

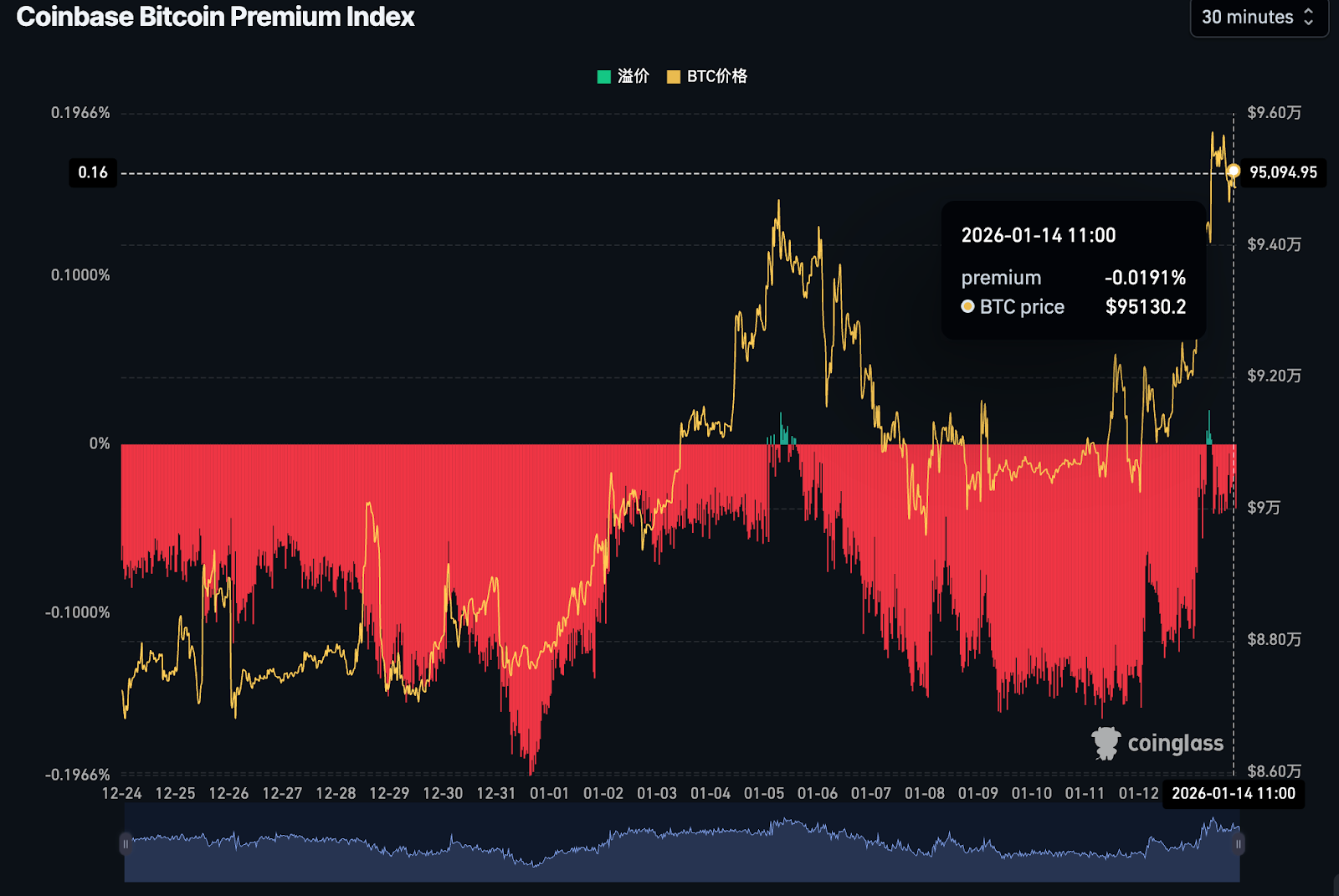

Bitcoin’s $95K test: Breakout or false dawn?

Bitcoin’s $95k push is a conditional breakout. While inflation is easing, analysts say the rally still lacks the spark of strong US demand.

Bitcoin’s push above $95,000 looks impressive, but this rally is best viewed as a conditional breakout rather than a clean escape. Prices have surged on easing US inflation and improving global liquidity, yet one crucial ingredient remains missing: strong US demand. Without it, the move risks stalling rather than accelerating.

That tension sits at the heart of the current market. Global investors are buying into the macro narrative, while derivatives traders are being forced out of bearish positions; however, American spot participation remains subdued. Whether Bitcoin can turn this surge into a sustained trend now depends less on momentum and more on who steps in next.

What’s driving Bitcoin’s latest move?

The immediate catalyst came from cooler-than-expected US inflation data, which reinforced expectations that the Federal Reserve will continue cutting rates this year. Lower inflation eased pressure on Treasury yields and loosened financial conditions - a combination that has historically supported Bitcoin and other risk assets.

Political uncertainty amplified the reaction. Reports that the US Justice Department issued grand jury subpoenas linked to the Federal Reserve unsettled markets and weakened the dollar. That pushed investors towards assets perceived as insulated from central-bank risk. Bitcoin rose more than 4% in response, while ether, solana, and cardano jumped between 7% and 9% in a single session.

Why it matters

US demand has historically been the key factor in determining whether temporary rallies or lasting bull phases emerge. When American capital engages, price strength tends to persist. When it does not, upside moves often rely on leverage and overseas flows, making them more fragile.

According to Singapore-based crypto exchange Phemex, a negative Coinbase premium indicates “strong selling pressure and potential capital outflows from the US market”.

That warning is significant because the premium turned negative shortly after the US election in November 2024 and has largely remained there, even as Bitcoin’s price climbed.

One explanation lies in regulation. US investors appear to be waiting for the Clarity Act, proposed legislation aimed at clarifying crypto oversight. The Senate delayed a crucial markup until late January to secure bipartisan backing, keeping institutional investors cautious despite favourable macro conditions.

Impact on crypto markets

The rally has already reshaped positioning. More than $688 million in crypto derivatives positions were liquidated in a single day, with short sellers accounting for roughly $603 million of that total. Nearly 122,000 traders were wiped out as prices surged sharply.

That wave of forced buying helped propel Bitcoin past $95,000, but it also quickly rebuilt leverage. Open interest has risen as prices approach levels that previously triggered heavy selling. This combination - rising leverage near resistance - increases the likelihood of sharp, two-way volatility.

Beyond crypto, the broader market backdrop supports risk-taking. Asian equities have reached record highs, silver has broken above $90 an ounce, and gold is hovering just below all-time highs. Investors are increasingly positioning for looser financial conditions and currency instability rather than defensive outcomes.

Expert outlook

Most analysts agree that Bitcoin’s broader trend remains constructive, but the quality of the rally is now under scrutiny. Without renewed US spot demand, price gains may struggle to extend sustainably, even if global liquidity continues to improve.

Several strategists argue that approval of the Clarity Act could act as a release valve for sidelined US capital, potentially pushing Bitcoin towards fresh record highs. Until then, the market remains vulnerable to pullbacks driven by unwinds of leverage rather than fundamental shifts.

In short, Bitcoin is moving higher - but it is not yet being embraced by its most influential buyer base.

Key takeaway

Bitcoin’s surge above $95,000 reflects improving macroeconomic conditions and a global risk appetite, but it falls short of a decisive breakout. The absence of strong US demand leaves the rally dependent on offshore flows and leverage rather than conviction. Whether this move becomes the foundation for new highs or fades into consolidation will depend on regulation, spot inflows, and how the market handles rising leverage. The next signal to watch is not price, but participation.

Bitcoin technical outlook

Bitcoin is attempting to reassert bullish momentum after holding above the $84,700 support zone, with price now pushing back toward the $95,000 area. The rebound has lifted RSI sharply toward overbought territory, signalling strong short-term momentum but also raising the risk of near-term profit-taking.

Structurally, the broader recovery remains intact as long as BTC holds above $84,700; however, upside progress is likely to face resistance at $104,000, followed by $114,000 and $ 126,000. Sustained acceptance above current levels would support further upside, while failure to hold gains would keep Bitcoin range-bound rather than confirm a renewed trend higher.

Silver smashes past $90: Why the trend may be just beginning

Silver’s surge past $90/oz has analysts debating: is this a momentum spike or the start of a deep structural trend?

Silver has achieved more than just setting a new record, according to analysts. By surging past $90 per ounce for the first time in history, the metal has prompted markets to reassess whether this is merely a momentum surge or the early phase of a deeper, structural trend. Prices are already up more than 25% in 2026, pushing silver’s market capitalisation above $5 trillion and restoring its relevance across both macro and industrial narratives.

What makes this breakout stand out is the backdrop. Softer core inflation, rising expectations of Federal Reserve rate cuts, tightening physical supply, and growing geopolitical uncertainty are all reinforcing one another. When those forces align, silver rarely tops out quietly. The more important question now is not how silver reached $90, but whether the conditions driving it are strong enough to carry prices further.

What’s driving Silver?

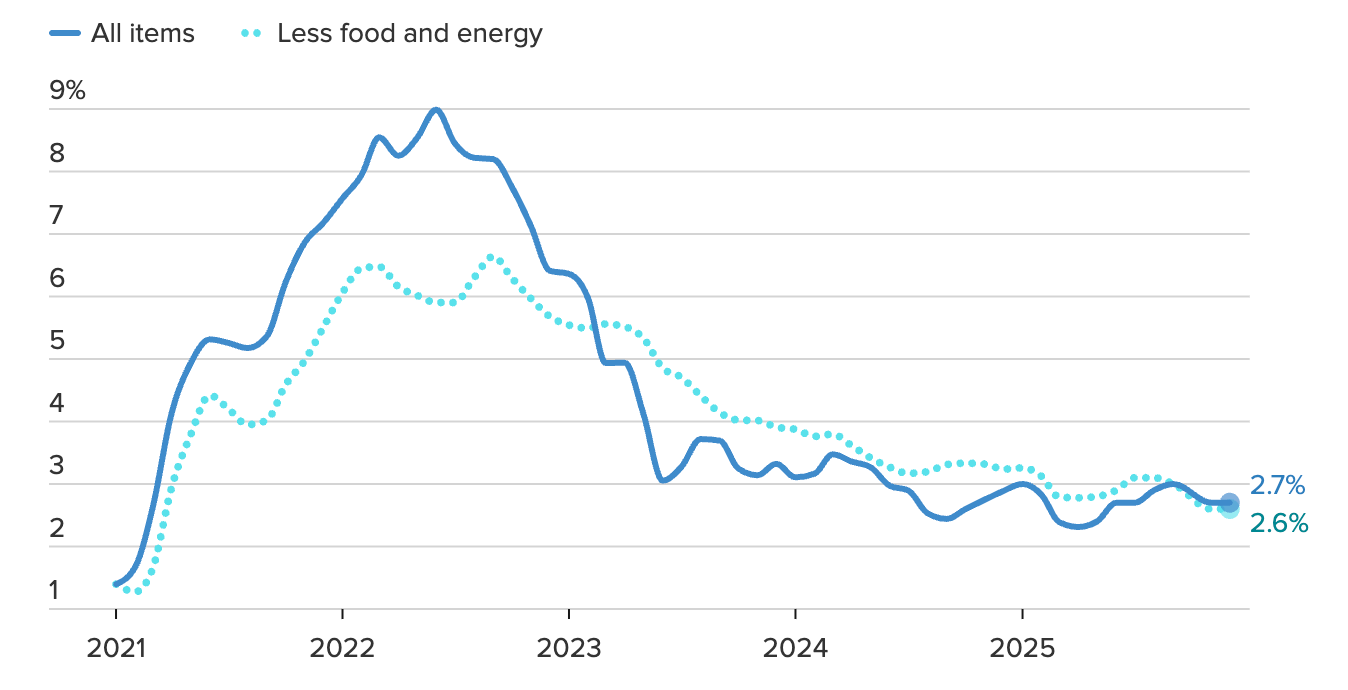

The immediate macro trigger came from U.S. inflation data that kept the disinflation narrative alive where it matters most. The Core CPI rose just 0.2% month-on-month and 2.6% year-on-year in December, slightly softer than expected, prompting markets to lean back into the idea that policy easing remains on the table in 2026.

Rate futures now price two Federal Reserve cuts this year, with growing conviction that easing could begin by mid-year.

That matters because silver, like gold, does not offer yield. When real yields fall, and cash becomes less attractive, the opportunity cost of holding precious metals drops sharply. A softer dollar adds another layer of support, pushing dollar-denominated commodities higher. Gold reacted first, breaking above $4,630, but silver followed with greater force as momentum funds and short-term traders accelerated the move through the psychologically important $90 level.

Geopolitics has injected a fresh layer of urgency into the rally. Escalating tensions involving Iran, alongside renewed criticism of the Federal Reserve’s independence from former US President Donald Trump, have triggered aggressive safe-haven flows into precious metals (Source: Reuters, January 2026).

During the Asian trading session, silver volumes surged to more than 14 times the daily average, while prices jumped over 7% intraday, a pattern consistent with institutional rotation rather than retail speculation, according to analysts.

Silver’s dual role as both a monetary hedge and an industrial input tends to amplify these moves relative to gold when political uncertainty spikes.

Why it matters

Silver’s rally is not just an inflation hedge. It reflects a broader shift in investor behaviour as confidence in policy predictability weakens. Political pressure on central banks, rising fiscal concerns, and ongoing geopolitical tensions have revived demand for assets that sit outside the financial system. Silver benefits from that shift, particularly when investors seek alternatives beyond gold.

What differentiates the current move is that safe-haven demand is colliding with structural scarcity. BMI Research forecasts that the global silver market deficit will persist through at least 2026, driven by strong investment inflows, robust industrial demand, and constrained supply growth. Unlike gold, silver lacks deep above-ground inventories that can easily absorb shocks. When demand accelerates unexpectedly, price adjustments tend to be swift and outsized.

This interaction helps explain why silver has outperformed gold during the rally. Analysts often describe silver as behaving like “gold on leverage” during periods of macro stress. When monetary uncertainty and physical tightness coexist, silver rarely moves quietly or briefly.

Impact on industry and markets

Rising silver prices are already being felt in industrial supply chains. Solar panel manufacturers, EV producers, and technology firms rely heavily on silver for conductivity and efficiency. The International Energy Agency estimates that global solar capacity could quadruple by 2030, potentially consuming nearly half of the annual silver output if current technologies remain dominant.

Financial markets are responding in parallel. Investment demand has surged, with silver ETFs seeing renewed inflows as investors seek exposure to both the metal’s macro hedge and its industrial growth story.

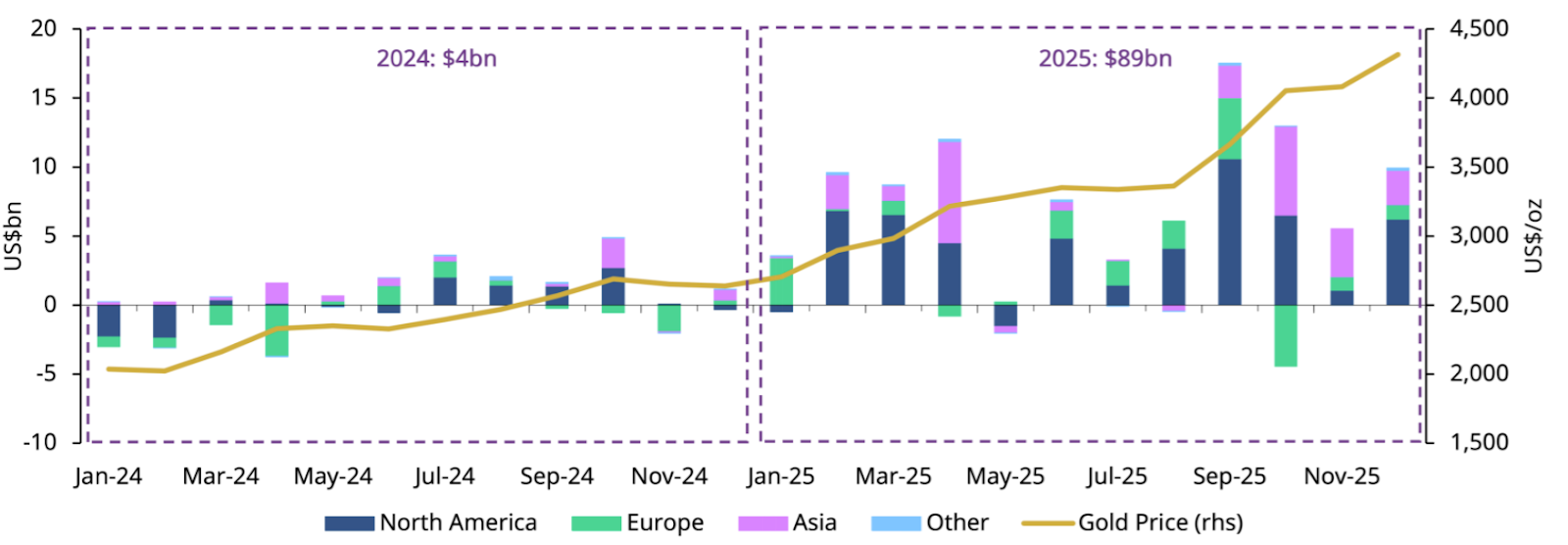

The World Gold Council estimates that physically backed precious-metal ETFs attracted $89 billion in inflows during 2025, the largest annual total on record. These flows tend to dampen downside volatility by providing a steady base of longer-term demand.

For consumers, the impact is less immediate but still meaningful. Higher silver prices increase production costs across renewable energy, electronics, and data infrastructure, reinforcing the inflationary pressures that initially drew investors to precious metals.

Expert outlook

The outlook for silver remains constructive, although volatility is expected. Silver has a long history of overshooting during momentum phases, often followed by sharp but temporary pullbacks. Those retracements, however, do not necessarily signal trend exhaustion when real yields remain under pressure and supply deficits persist.

Institutional forecasts are becoming increasingly assertive. Citigroup recently projected that silver could approach $100 per ounce within the next three months, alongside a gold target near $5,000, citing falling real yields, strong investment demand, and persistent supply constraints. With silver now trading within 10% of that level, such targets are no longer abstract and are actively drawing momentum and trend-following capital.

The key signals to watch are inflation trends, central bank communication, and labour market data. Any sustained re-acceleration in core inflation could delay rate cuts and trigger consolidation. Conversely, confirmation that disinflation is intact would strengthen the case for further upside. As long as uncertainty around growth, policy, and geopolitics remains elevated, silver’s role as both a defensive asset and an industrial input keeps the longer-term trend firmly in play.

Key takeaway

Silver’s move above $90 is more than a milestone. It reflects a convergence of softer inflation, rising rate-cut expectations, persistent supply shortages, and renewed demand for real assets. While volatility is inevitable, the forces behind the rally remain firmly in place. The next phase will depend less on headlines and more on whether macro conditions continue to erode confidence in cash and bonds.

Silver technical outlook

Silver is testing the prior swing high near $90.93, placing the market in price discovery mode close to an all-time high. At this stage, the move is extension-driven rather than retracement-driven, limiting the usefulness of Fibonacci levels.

The 78.6% retracement at $77.53 represents the first meaningful structural support; however, at approximately 14.5% below current prices, it remains too distant to guide near-term positioning.

Momentum signals point to late-stage trend conditions. RSI readings across multiple timeframes are firmly overbought, with short-term momentum more stretched than the broader trend. A moderate bearish divergence is emerging as price pushes higher while momentum begins to roll over - a common warning sign in commodities ahead of sharp consolidation or reversal.

Trend strength remains intact, with ADX confirming a strong uptrend, but extreme volume at new highs raises the risk of a blow-off move rather than a sustained breakout.

Upside follow-through requires sustained closes above the recent high with momentum holding firm. Failure to hold gains, fading volume, or a close back below the breakout zone would confirm exhaustion and shift focus toward consolidation or reversal.

Why Google’s Gemini–Apple deal is a defining AI moment

Gemini in Siri is a defining AI moment: the fight has moved from 'innovation theatre' to massive real-world distribution.

Google’s decision to embed its Gemini models into Apple’s Siri is a defining AI moment because it shifts the battleground from innovation theatre to real-world distribution. Instead of competing for attention through standalone chatbots, Alphabet has secured a position inside Apple’s ecosystem of more than two billion active devices, placing its AI where consumer behaviour actually happens.

Markets reacted calmly, with Alphabet shares rising around 1% and Apple edging 0.3% higher after hours. Yet the significance runs far deeper than the initial price move. This agreement marks a new phase in artificial intelligence, where scale, integration, and trust take precedence over who ships the flashiest model first.

What’s driving Google’s Gemini push?

At its core, this deal reflects Google’s long-standing strategy: win through infrastructure, not spectacle. While rivals race to dominate headlines, Alphabet has focused on embedding Gemini across cloud services, enterprise tools, and now the world’s most influential consumer hardware platform. Siri’s revamp gives Google an AI distribution channel that no advertising campaign could buy.

The economics of artificial intelligence also explain the timing. Training and deploying frontier models demands vast compute resources and specialised chips, areas where Google already operates at an industrial scale. As chipmakers prioritise AI data centres over consumer electronics, control over reliable AI infrastructure becomes a competitive moat rather than a cost burden.

Crucially, Apple’s endorsement validates Gemini’s maturity. Apple confirmed that Gemini will power the next generation of Apple Foundation Models, while Apple Intelligence will continue to run on-device and through its Private Cloud Compute framework, preserving strict privacy standards. That balance between capability and control is increasingly decisive in AI partnerships.

Why it matters

For Alphabet, the agreement reframes its role in the AI race. This is no longer about whether Google can build competitive models; it is about whether it can quietly become the default AI layer across platforms it does not own. Parth Talsania, CEO of Equisights Research, described the move as one that “shifts OpenAI into a more supporting role,” underscoring how distribution can outweigh pure model branding.

Investors care because distribution converts experimentation into revenue. AI embedded into everyday tasks creates steady demand for cloud compute, enterprise services, and long-term monetisation opportunities. Alphabet now reaches Apple’s premium user base, a segment that historically sat outside Google’s deepest ecosystem.

The deal also challenges a persistent market narrative that Apple is “behind” in AI while Google struggles to monetise it. In reality, both firms are leaning into their strengths, creating a partnership that reduces execution risk for each.

Impact on the AI and smartphone markets

The immediate effects will be felt in smartphones, where AI is becoming the catalyst for the next upgrade. Global handset shipments increased by 2% in 2025, with Apple leading the market at a 20% share. A smarter, Gemini-powered Siri offers Apple a clearer justification for upgrades at a time when hardware improvements alone are no longer enough.

For Google, the implications stretch well beyond handsets. Each AI-driven interaction routed through Gemini increases demand for Google’s cloud infrastructure, reinforcing a feedback loop between consumer usage and enterprise revenue. That dynamic becomes especially valuable as AI workloads intensify competition for chips and data-centre capacity.

The concentration of influence has not gone unnoticed. Tesla CEO Elon Musk warned publicly of “an unreasonable concentration of power for Google” following the announcement. Whether or not regulators act, the comment highlights how decisively Alphabet has positioned itself within the AI value chain.

Expert outlook

Analysts broadly view the partnership as a structural win rather than a short-term trade. Wedbush’s Daniel Ives reiterated his positive outlook on Apple while noting that Google stands to benefit from sustained AI and cloud demand into 2026 and beyond.

Earnings expectations support that view. Alphabet’s consensus forecasts have risen steadily over the past year, driven by AI-led cloud growth and improving monetisation. The remaining uncertainty lies in execution, specifically in terms of performance consistency, regulatory scrutiny, and Apple’s ability to deliver the upgraded Siri on schedule.

Investors will focus on Apple’s upcoming earnings call for clarity on the rollout, while Alphabet watchers will track whether Gemini-driven workloads translate into accelerating cloud revenues.

Key takeaway

Google’s Gemini–Apple partnership marks a shift from AI hype to AI infrastructure dominance. By embedding its models into Siri, Alphabet secures distribution, data flow, and long-term monetisation potential. The market reaction may have been muted, but the strategic implications are not. The next test will be execution, regulation, and whether this integration delivers tangible value to users.

Alphabet technical outlook

Alphabet has pushed decisively into price discovery, breaking above prior resistance and extending its bullish trend with strong upside momentum. The move reflects sustained demand, but momentum indicators suggest conditions are becoming stretched: the RSI is rising sharply into overbought territory.

Structurally, the trend remains firmly constructive as long as price holds above the $300 zone, which has flipped into a key support area after previously capping gains. A deeper pullback could come into focus below $280, while sustained acceptance above current levels would maintain the upside bias, even if short-term pauses emerge as the market digests its gains.

Traders tracking these moves can analyse Alphabet and Apple price action in real-time on Deriv MT5, where advanced indicators, multi-timeframe charts, and US tech stocks are available on one platform.

“No one’s above the law”: Jerome Powell’s defiant stand against the Oval Office

Jerome Powell has spent years speaking in the measured, cautious tones of a career diplomat. As the steward of the world’s most powerful central bank, his words are usually designed to calm markets, not ignite them. But on Sunday, 11 January, the mask slipped.

Jerome Powell has spent years speaking in the measured, cautious tones of a career diplomat. As the steward of the world’s most powerful central bank, his words are usually designed to calm markets, not ignite them. But on Sunday, 11 January, the mask slipped. In a video statement that sent shockwaves through the financial world, Powell accused the Trump administration of "pretextual" legal warfare.

As per Bloomberg, this isn't just about a $2.5 billion office renovation; it’s about a President demanding loyalty from a man sworn to be independent. Today, the legendary "Fed Put"—the market's long-standing belief that the central bank would always step in to save the day—has been replaced by a "Fed Probe."

The pretext: A $2.5 billion renovation

The spark for this historic conflagration, on the surface, is a dispute over real estate. The Department of Justice (DOJ) served the Federal Reserve with grand jury subpoenas on Friday regarding a decade-long project to modernise its Washington D.C. headquarters.

However, Powell isn’t buying the "oversight" narrative. In a blunt video address, he described the investigation as a "pretext" aimed at forcing his hand on interest rates. According to Reuters, Powell argued that the threat of criminal charges is a direct "consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President."

Trump’s populist push: lighting the fuse

The timing is no coincidence. In the back half of last week, President Trump dramatically ramped up his populist economic messaging in a bid to juice markets in an election year - moves that, paradoxically, may have helped trigger the sell-off now unfolding.

Among the proposals floated or ordered:

- Directing “his representatives” to buy mortgage-backed securities to push borrowing costs lower

- Banning institutional investors from buying single-family homes

- Floating a one-year 10% cap on credit-card interest rates - with no enforcement detail

For fund managers, this wasn’t stimulus. It was policy improvisation. And when combined with renewed attacks on the Fed, it raised a red flag: political interference in the plumbing of the financial system.

As one strategist put it privately: Trump wants higher stocks now, but attacking Fed independence is one of the fastest ways to scare off the very capital that supports them.

Market mayhem: Gold soars, dollar dips

The financial markets reacted with immediate and visceral alarm. The "institutional risk premium"-the cost investors pay for political instability - is suddenly front and centre.

- Gold’s historic Run: According to The Straits Times, spot gold prices hit an unprecedented record of $4,563.61 per ounce as investors fled for the ultimate safe haven.

- Greenback under fire: The US dollar index fell 0.3% to 98.899, according to Reuters, as confidence in the autonomy of the world’s reserve currency wavered.

- Futures in the red: US stock futures tumbled, with the Nasdaq-100 shedding 0.6% in early trading as the tech sector braced for a more volatile interest rate environment.

Why gold is surging

Gold’s surge isn’t about technicals anymore, according to analysts. It’s about trust.

Even with gold flashing overbought signals, demand continues to build. Why? Because the list of macro risks keeps growing:

- Political interference in monetary policy

- Rising geopolitical tensions, including reports of potential US action in Iran and escalating Arctic positioning by the UK and Germany

- Rate-cut uncertainty ahead of key US CPI data

As analysts note, gold thrives when rules feel flexible and institutions feel vulnerable. And right now, both boxes are ticked.

Silver: same tailwinds, sharper edges

Silver, meanwhile, is riding the same macro wave - but with extra volatility.

Its dual identity matters. Safe-haven flows support silver alongside gold, but industrial demand adds fuel when growth narratives resurface. That combination makes silver powerful - and dangerous.

Analysts warn that silver rallies often attract fast money. When sentiment shifts, exits can be just as violent. For investors, silver remains compelling, but timing matters far more than it does with gold.

The stakes: Autonomy vs. allegiance

This isn't just a legal battle; it’s a constitutional crisis in slow motion. As noted by Maybank strategist Fiona Lim in The Straits Times, the administration’s pressure suggests a desire to install a "loyalist" when Powell’s term expires in May.

"Powell has had enough of the carping from the sidelines and is clearly going on the offensive," Ray Attrill, head of FX strategy at National Australia Bank, told Reuters. By moving the fight into the public eye, Powell is betting that the market’s fear of a politicised Fed will be a stronger shield than any legal defence.

Key takeaway

For investors, the playbook has changed, according to analysts. The Fed is no longer just fighting inflation; it is fighting for its very existence as an independent body. As Saxo Markets analysts pointed out, the "open warfare" between the Fed and the White House has introduced a level of volatility that hasn't been seen in decades.

Whether this ends in a courtroom or a boardroom, one thing is clear: the era of the "measured" Fed is over, according to analysts. The era of the “defiant” Fed has begun.

Gold technical outlook

Gold is extending its bullish advance, pushing into fresh highs near the upper Bollinger Band and reinforcing the strength of the underlying trend. The rally remains well-supported by momentum indicators, with the Relative strength index rising smoothly toward overbought territory, signalling strong buying pressure rather than an exhausted move.

While the pace of gains suggests the risk of near-term profit-taking is increasing, the broader structure remains firmly constructive. As long as price holds above the $4,035 support zone - and more importantly above $3,935 - any pullback could be corrective rather than trend-breaking.

Sustained strength above current levels could keep the upside bias intact, while consolidation would allow momentum to reset without undermining the broader bullish narrative. There is always the risk of price action surprising and doing the unexpected, traders should beware. You can monitor these levels with a Deriv MT5 account.

Why defence stocks are back in focus after Trump’s budget shock

Defence stocks snapped back into the spotlight after President Donald Trump signalled a dramatic shift in US military spending.

Defence stocks snapped back into the spotlight after President Donald Trump signalled a dramatic shift in US military spending. In a social media post that caught markets off guard, Trump floated a $1.5 trillion defence budget for 2027, a sharp jump from the roughly $901 billion set for 2026. The proposal triggered a rapid after-hours rebound in major US defence names, reversing earlier losses.

Lockheed Martin surged 7%, while Northrop Grumman climbed 4%, underscoring how tightly defence valuations remain tied to political direction. With markets already uneasy about stretched tech valuations, Trump’s comments have reignited interest in defence as both a policy-driven and geopolitical trade.

What’s driving defence stocks?

The immediate catalyst was Trump’s promise to build what he described as a “Dream Military”, backed by a significantly larger defence budget. The scale of the proposed increase matters. A move towards $1.5 trillion would represent one of the largest step-ups in US military spending outside wartime, reshaping long-term revenue expectations for defence contractors.

Earlier in the session, defence shares had sold off after Trump criticised contractors for prioritising dividends and share buybacks over investment in production capacity. That rhetoric briefly raised fears of tighter oversight and limits on capital returns. The swift reversal later in the day showed that investors remain far more sensitive to spending signals than to governance concerns, particularly when multi-year contracts are at stake.

Beyond Washington, defence demand remains structurally supported. Europe continues to rearm, NATO spending targets are rising, and conflicts in Ukraine and the Middle East have reinforced the political urgency of military readiness. These forces have made defence stocks increasingly resilient to broader market volatility.

Why it matters

Defence stocks occupy a unique position in equity markets. Unlike most cyclical sectors, their revenues are directly linked to government budgets rather than consumer demand or credit conditions. When spending expectations rise, earnings visibility improves almost instantly, even if actual contracts take years to materialise.

Analysts argue this is why defence stocks now trade more like political assets than industrial ones. “Markets are pricing defence on policy momentum, not balance sheets,” a US defence strategist told Reuters. “Once spending direction is clear, the sector reprices very quickly”.

For investors, that dynamic increases both opportunity and risk. Sudden changes in rhetoric can trigger sharp moves in either direction, making timing and positioning more important than traditional valuation models.

Impact on markets and sector rotation

The renewed interest in defence comes as signs of fatigue emerge in the semiconductor and AI-led rally that dominated early 2026. Chipmakers drove gains at the start of the year, but concerns over valuation and profit sustainability have prompted a gradual rotation. Defence stocks are now absorbing some of that capital, supported by clearer fiscal tailwinds.

Performance data reflects the shift. Lockheed Martin is up nearly 8% year to date, while Halliburton has gained 12%, benefiting from both defence and energy-linked demand.

In Europe, defence heavyweights such as BAE Systems and Rheinmetall have posted strong gains, driven by persistent geopolitical headlines.

Options markets suggest investors expect larger swings ahead. Implied volatility across defence names has risen, echoing patterns seen in early 2022 when geopolitical escalation sent European defence stocks sharply higher. Rheinmetall’s 30% surge in a single week following the Ukraine invasion remains a clear historical parallel for how quickly the sector can reprice.

Expert outlook

Looking ahead, defence stocks face a familiar mix of optimism and uncertainty. Trump’s proposal still requires political backing, and budget negotiations could dilute the headline figure. However, even a partial increase would mark a meaningful shift in spending priorities relative to recent years.

Strategists expect defence to remain a headline-driven trade in the near term. Some favour options-based strategies to manage rising volatility, while others see value in pairing defence exposure against shorts in overextended tech sectors. The common thread is caution around chasing rallies without policy confirmation.

Key signals to watch include Congressional responses, NATO spending updates, and any clarity on how tariff revenues might be used to fund defence expansion. Until those questions are answered, defence stocks are likely to remain sensitive to every policy headline.

Key takeaway

Defence stocks are back in focus as Trump’s budget proposal reshapes market expectations around military spending. The rapid rebound highlights how tightly the sector is tied to political direction rather than short-term earnings. With signs of rotation away from AI, defence could remain a dominant theme in 2026. Investors should monitor budget negotiations and geopolitical developments for confirmation.

Lockheed Martin technical outlook

Lockheed Martin has surged sharply from the $480 support zone, briefly testing the $540 resistance before encountering aggressive profit-taking. The move highlights strong upside momentum, but the swift rejection near resistance suggests the rally may be entering a digestion phase rather than extending immediately. Momentum indicators reflect this balance: the RSI has risen rapidly toward overbought territory, signalling strong bullish participation but also increasing the risk of near-term consolidation.

Structurally, holding above $480 maintains the broader bullish bias, with deeper downside risk only emerging below $440. A sustained break above $540 would be needed to confirm trend continuation, while consolidation near current levels would be consistent with the market absorbing recent gains.

Sorry, we couldn’t find any results matching .

Search tips:

- Check your spelling and try again

- Try another keyword